Draws & Deals — Week №31 Review

Welcome to the weekly, a regular update on inventories, themes, and factors we are watching, in the physical, paper, and equity markets — and what a fun little week it was in Calgary — we got a big asset transaction, a new public player, a huge crude draw — and the weather was nice the entire time.

On the macro front, we got mixed economic data, with ISM PMI edging higher (though, missing expectations, and still contractionary), while data prints out of China were equally weak with housing sales falling, business confidence shrinking, and general infrastructure spending remaining weak. On the bullish side of things, Saudi Arabia pledged to extend their 1mb/d output cut for another month, and Russia has agreed to a 300kb/d output cut for September (compared to 500kb/d of cuts currently, is how we interpret this release).

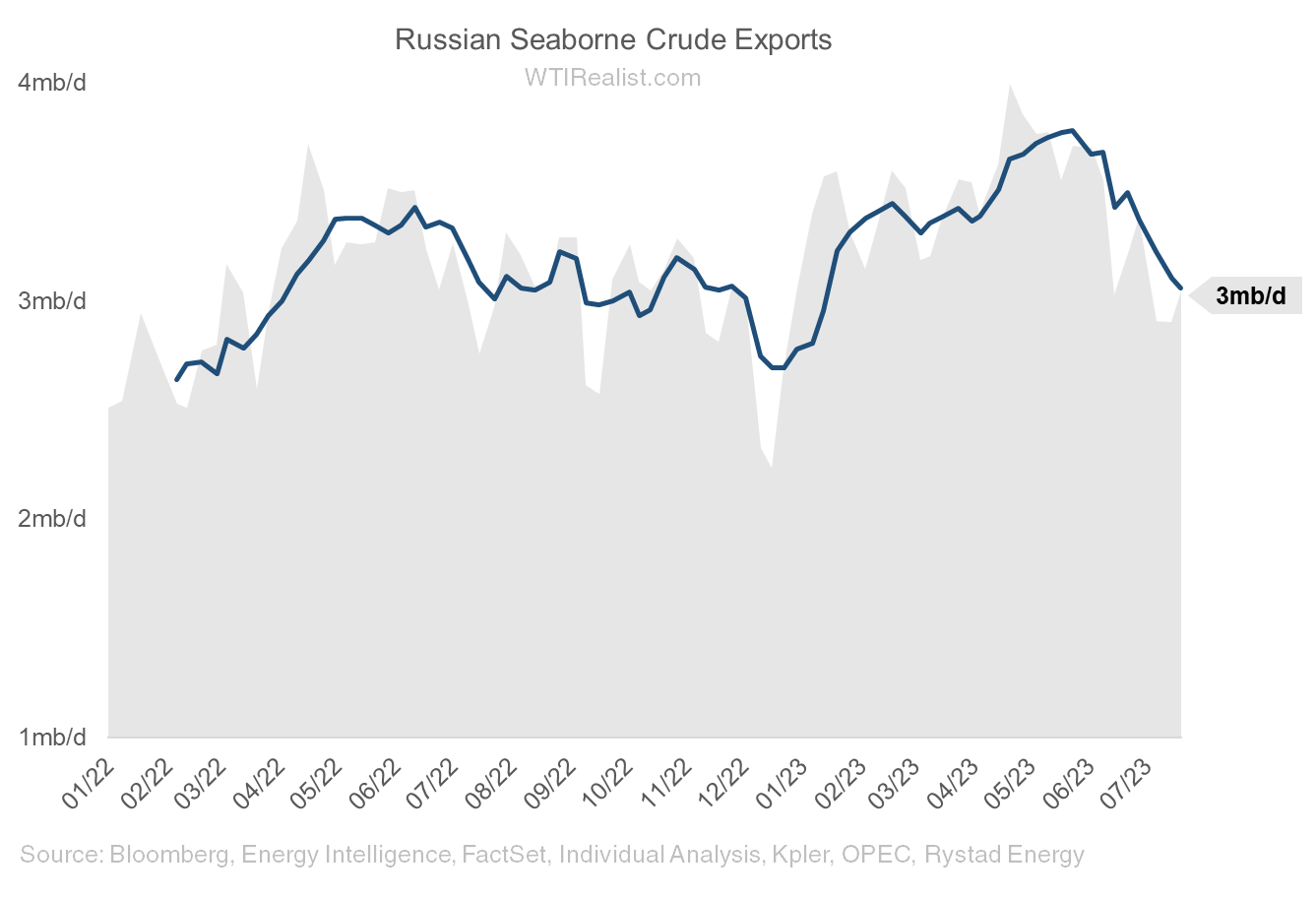

Last week, Russian seaborne exports ticked up slightly, though the 6 period moving average is assuredly lower. Thinking further about Russia this week, we see it as mostly immaterial to the short-term outlook, both bearish and bullish. Their exports to China will continue to flow, and China will continue to balance the market. Medium to longer term, the rolling of Russian production is undoubtedly bullish, but we believe the price of crude will reflect that slowly, then all at once (we’ve been fooled too many times by them), in the short term we think that Russian production uncertainty is priced into crude, especially consider the spare capacity among the Gulf producers, missing Russian barrels are nowhere as alarming as last year (and the magnitude of the possible loss is much less this year). Additionally, incremental export/production losses, above the 500kb/d pledged during the summer we view as unlikely. Confirmation that Russian production is rolling, would be (as discussed earlier this week) a much needed bullish support over the coming few years, but short term (i.e. how are we navigating the second half), the Russia risk feels bearishly slanted (if those barrels do come back) and mostly immaterial to prices.

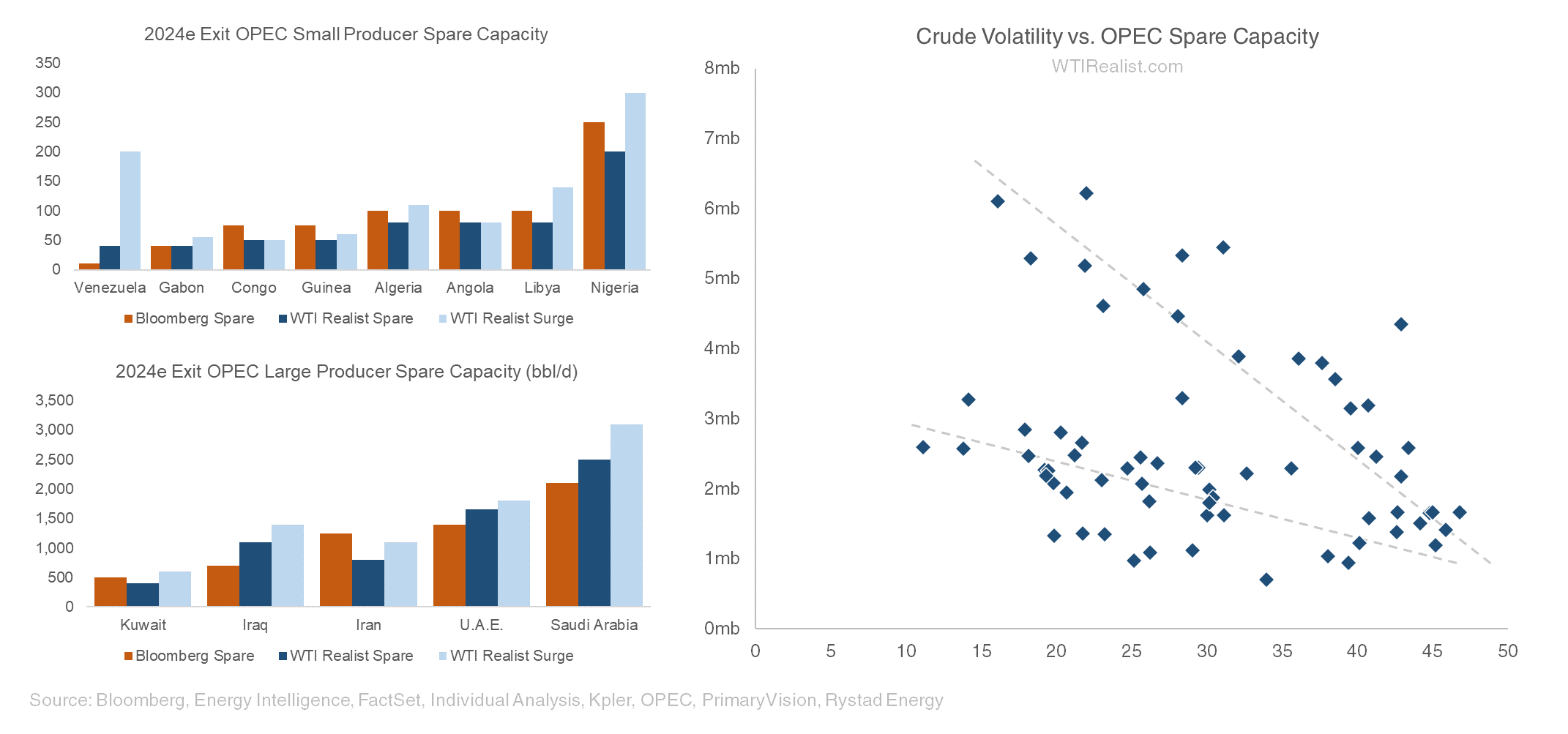

We will see how exports progress, but so far, we are not continuing to trend lower on the weekly outlook. Given our spare capacity outlook, really we do believe that we see two realities coming soon — lesser volatility (an OPEC desirable outcome), and, consistently range bound prices (remember, we think it’s a “healthy market”) — and during the next 16 months, we think there’s >5mb/d of spare capacity the Gulf producers will accrue. This serves to make the Russian possibilities even less material. Really, most of our work is determining what’s “material”, and we’ve called US, and Russia immaterial now, owing to strong international growth (ex-OPEC) and strong OPEC spare capacity that should last the market a good length of time.

While Chinese commercial inventories continued to build, global commercial inventories started their long awaited roll. Global inventories draining is obviously bullish (though again, we reiterate our work on how much inventories have to churn before we see a significant price response), and think we are in a draw regime where prices will be less reactionary to huge global draws (these soft price reaction eras tend to happen when inventories are high, but spare capacity is strong).