Back From Break

Both the blog, and crude oil

While the second half has started with a bang (or rather, a crude rip) — it has been, pretty well, in line with everyone’s expectations. Almost poetically, oil started its move upwards on June 27th, and has been uncannily up and to the right, since the start of the month. So there are lots of narratives floating around — we’d tend to lean bullish, though cautiously, and in a smorgasbord of a catch up note today, we walk through and expand on key market happenings over the past month, and factors to monitor. Note, and the end, we have published a research schedule (we’ve now hired a part-time analyst which will help improve our product offerings, and frequency) along with our equity ideas going forward, which will be covered in future notes.

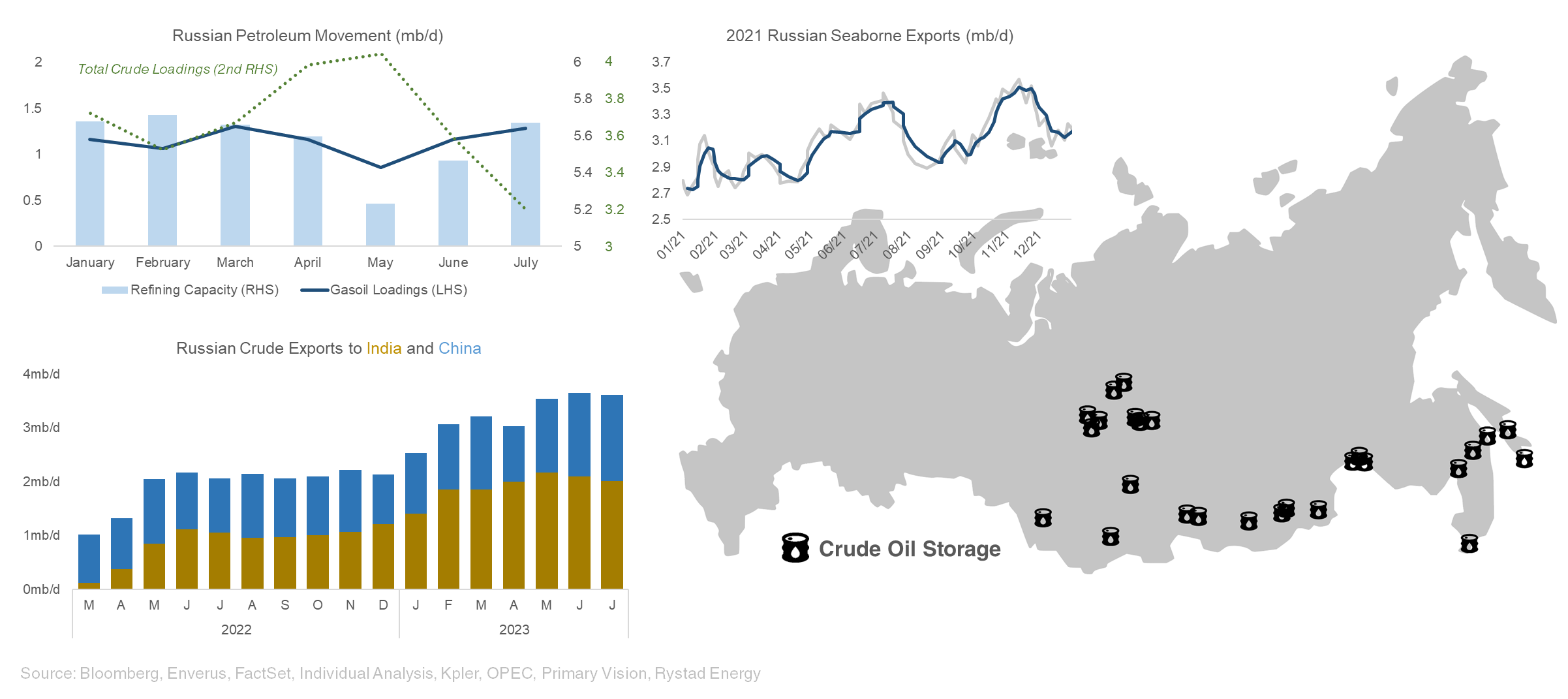

Russia is important to watch here, we are clearly seeing crude loadings fall, as promised, though we are seeing product exports increase (not quite at a 1:1 ratio), as refineries come back online. Prior to the war, crude exports typically would drop into the later summer (favouring products), then ramp into the winter. There is a chance that the softening of Russian exports is seasonal, though a persistent falling of seaborne exports, would likely mean the start of a production decline in the country.

Understanding Russia’s storage situation is important. Most of their working storage is located in their western Siberian fields, and then continues east along the ESPO pipeline link to China. Transneft holds a small amount of slack pipeline storage, but, in general, Russia is short storage. It has been said that Russia drew down their storage in their 2Q23 export push, so, we are looking to see 3-4 months of sustained seaborne export decline. Note, that shipments from the arctic port of Murmansk, and the eastern ports of Kozmino, and Sakhalin have continued without softening into July. This morning was saw Bloomberg report that total meters drilled was up 5% month on month in June, so while we are hopeful that exports start to decline, we are not holding our breath, with the possibility that decreased exports from western ports are filling storage in the east, and increased feedstock demand is clearing the balance that storage may not be able to take. If we see a flattening, or slight increase of Russian exports, it would be bearish, but the takeaway here, is flat to declining exports, in our opinion, would be the actual start of Russia’s production struggle. After SLB finally stopped equipment shipments to Russia, it will be incrementally harder to maintain flat output. After a year and a half of general prognostication of Russia’s final production softening, we are watching close for signs of fight here.

Bullish for both producers, and the overall market, we’ve seen NGL prices recover significantly over the past few weeks, which is short term constructive for producers, though improves drilling economics significantly. The US dollar index continues to move lower (and the use of ‘dollar milkshake' practically disappearing, thank god) we see the possibility of a reacceleration of ISM PMI. The EIA also printed a positive demand revision this morning, countering some of the recession narrative that the street (and us, also) have bought into. Given that most of the recession narrative is gone, and the overall end of year S&P targets imply upside from here, equities certainly feel a bit more ownable than a few months ago.

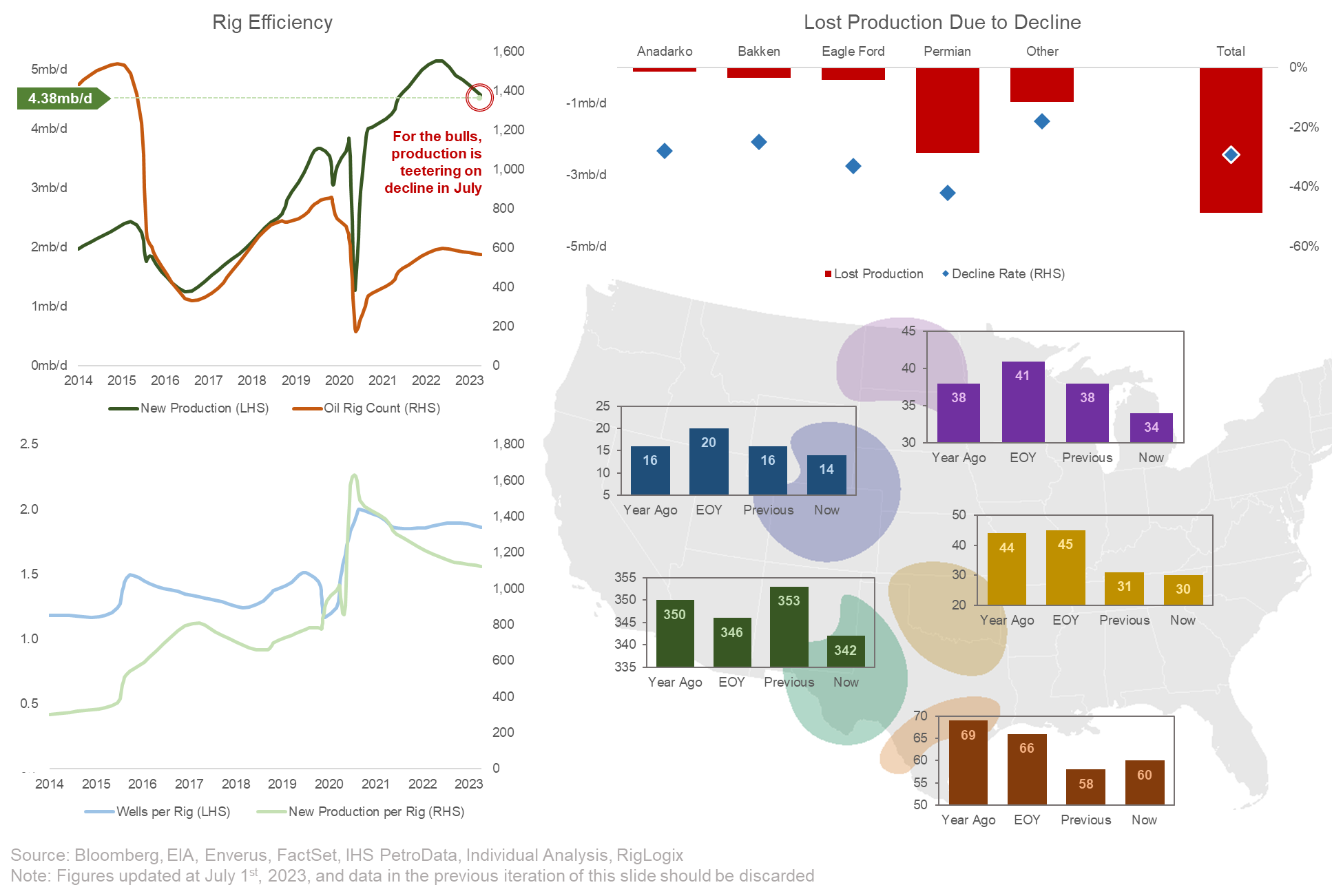

Quite bullishly, US production has started to turn the corner, and, for now, will likely print some consecutive month on month declines. This should put some wind into the sails of any and all bullish oil headlines over the next few months. We believe (and will introduce this into coverage next week) that US production is not going to continue to trend meaningfully lower for a long time, as long as crude stays above $70/bbl, though, given the pace of rig drops, and the time we spent below $70/bbl — it’s expected that US production will decline slightly through the remainder of the summer. As the Permian continues to work through some of its local issues, we believe this trend will reverse, and growth (albeit, much slower than 2014-2017) will continue. A continued, key theme is that price drives inventory and growth, for the most part, E&Ps that are liquids focused, have plenty of free cashflow to absorb acreage degradation, especially so at $80-90/bbl — and it’s expected that secondary basin growth will slowly recover in a $80/bbl environment.

On the bearish side (of course, this can’t be all bullish) — it’s our opinion that some of the Saudi export cuts is seasonal demand pulling barrels to be consumed locally, and we will see some easing of their “cuts” into year end as they turn to export those barrels. We are also seeing Chinese medium-sour-in-tank basis to an OPEC basket turn positive, which should encourage draws. Last week, there was also (again, reported by Bloomberg) discussions of restarting Kurdish pipeline exports through Turkey, which would add ~250kb/d to the market (accounting for currently smuggled production). Flaring events in Iran indicate that production continues to edge higher, and Chinese oil imports from Malaysia (a proxy for illegal crude from Venezuela, and Iran) have reached all time highs.

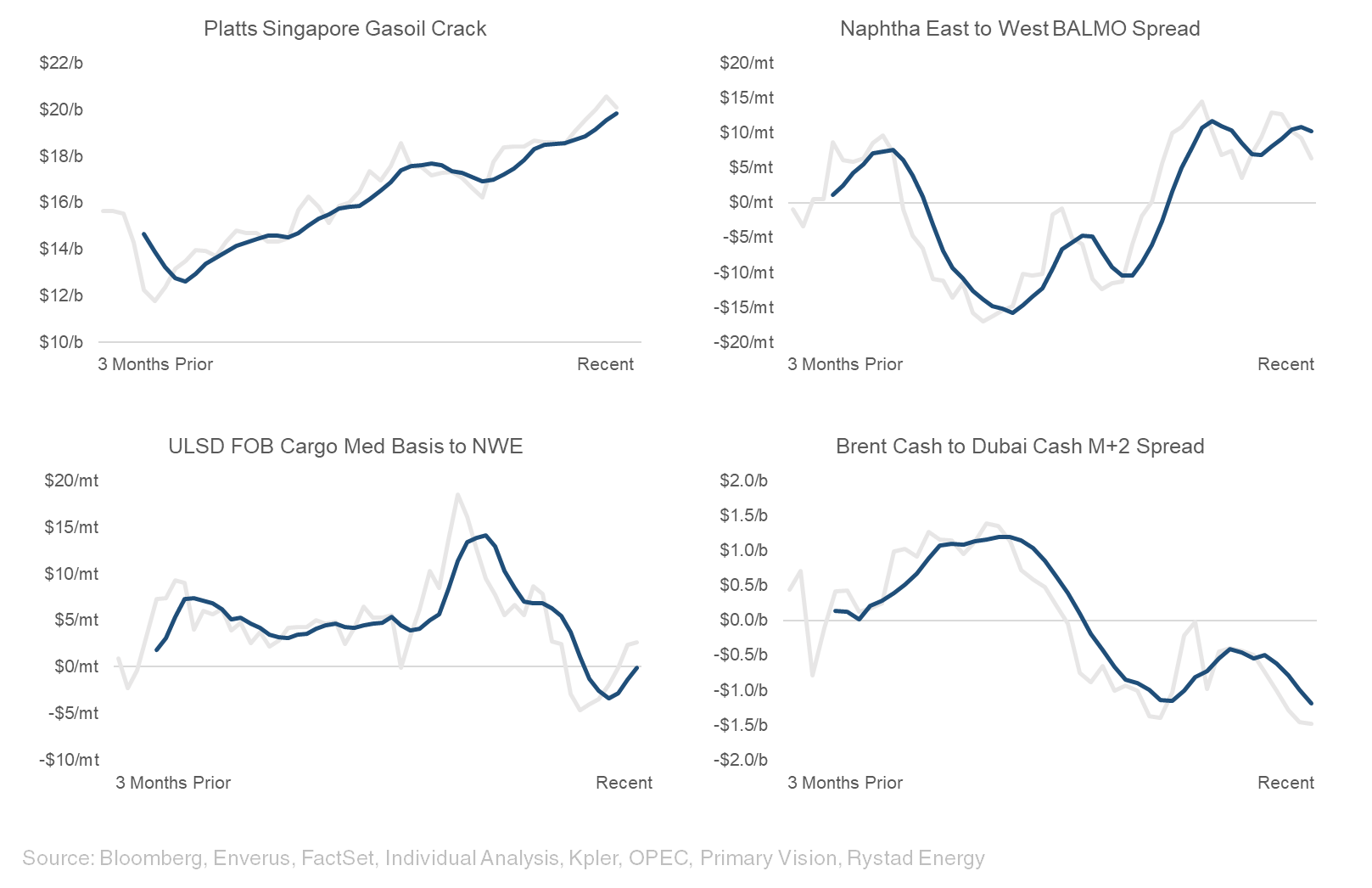

Some of the key arbs that we track are sending mixed messages — Singapore gasoil cracks are on fire as Singapore distillate inventories start to draw, and there is strength again in the east to west naphtha arb — and in general naphtha prices. There has been some screwy movement in diesel basis thanks to Russian exports, though, most importantly, Brent cash to Dubai cash spread is now negative, which isn’t encouraging to those (the bulls) that are hoping for west of Suez inventories to draw. All things considered (including time spreads, which have also turned supportive) this skews slightly bullish, but again, plenty of reasons to keep expectations in check.

This isn’t a market where the production isn’t there, as was assumed during last year’s pandemonium. There is an abundance of spare capacity throughout OPEC, and while, yes, they have buoyed the market with production cuts, it would be simply trite to think that production will not return to the market should prices surge too high (again, part of our hesitation to bring our H2 average closer to $85/bbl). Retail cracks are also significantly higher than H1, so we also think that OPEC (and on the tail, the Biden administration) may be a bit quicker to intervene. I continue to urge everyone to view the oil market as such, with times to total abnormality, simply, cut out. This gives much better perspective when deciding what to anchor to in any sort of look-back. Shockingly — we don’t think $130/bbl is a reasonable target, really, even $100/bbl is not a realistic target for any serious period of time, in our view. Not that demand can’t support it, but there is enough production that comes seriously into the money at $100/bbl that we must underwrite a significant supply response (see: 2022).

Going forward, we break down the narratives and review all the crude market factors that are pushing things higher, and lower — including; product cracks, inventories, local demand, tanker movements, spare capacity, rig counts, international growth, dark barrel exports, sector weightings, funds flows, shale degradation, China’s role in the market, time spreads and cash markets, manufacturing expectations, dollar strength, and, whatever else comes to mind. There’s truth in the whole price drives narrative discussion, and while, it’s certainly a bullishly slanted market, we really don’t see triple-digit prices in the cards — in fact, we would strongly reiterate our $78/bbl 2023 guidance (an implied second half price of $81.13/bbl) as we see some of the legs crude has grown so far this month, at risk as Iraq, and KSA possibly reintroduce supply back into the market, and as China risks destocking.

We will continue to be objective as possible.

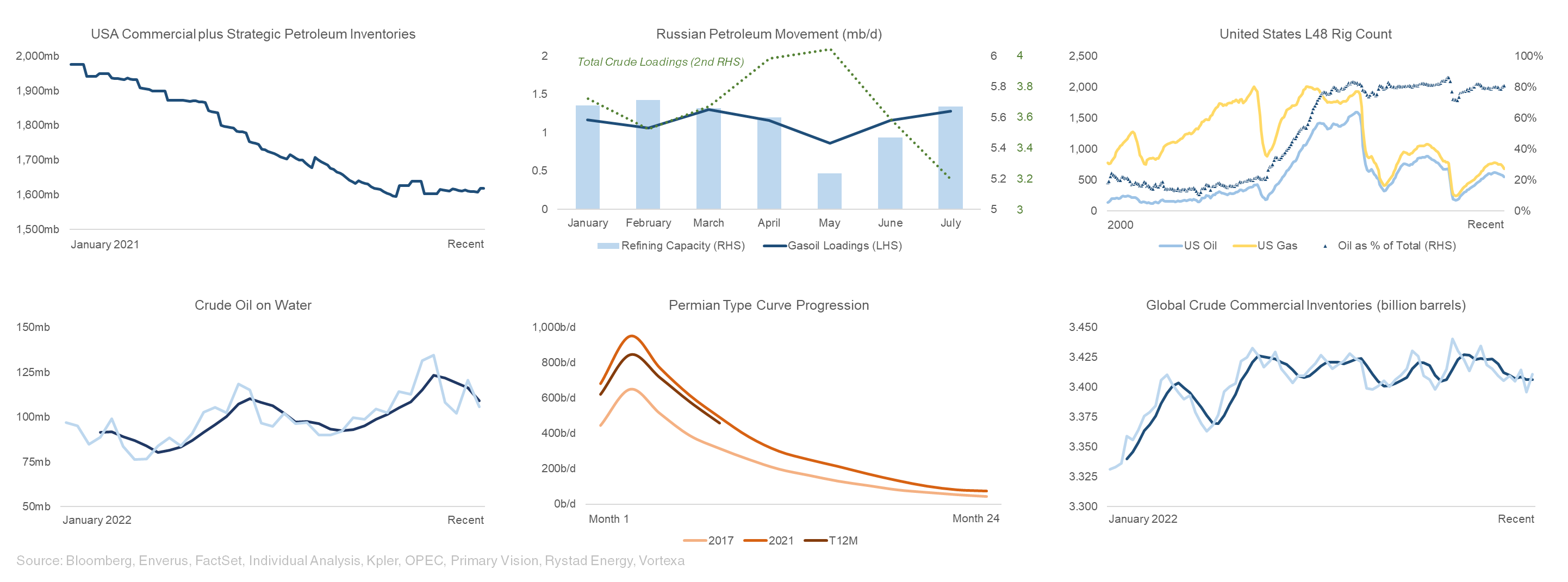

If you’re bullish, inventories are much lower than a year prior indicating perhaps imminent market tightness, if you’re bearish, the SPR doesn’t count as commercial inventory, and the pace of draws has slowed materially, indicating an implied balance.

If you’re bullish, Russian crude loadings are down materially since may (almost 1mb/d) — if you’re bearish, those volumes are showing up in product exports.

If you’re bullish, lower rig counts obviously means slowing production growth, though if you’re bearish, you can make the argument that the rigs being dropped are the least productive ones, and growth may continue to cling to life.

If you’re bullish, oil on water is rolling over, which means global, total observable inventories are drawing — and if you’re bearish, you’re making the case that that oil on water is filtering into the Sumed, and is just becoming onshore inventory.

If you’re bullish, productivity gains are clearly over, though if you’re bearish, the rate at which productivity is rolling over isn’t conducive to the “Permian is almost dead” thesis which has been a short-term catalyst for many.

If you’re bullish, inventories are starting to draw, and are nearing their lowest since 1Q23, though if you’re bearish, local inventories (such as the US) are drawing, while global commercial inventories have not really rolled over yet.

Though, on the double bullish upside, the Chinese stimulus story has started to unfold, which should continue to induce demand in the east, though, we think that they have reached peak import growth pace, and it will soften, or decline slightly into the end of the year. While some commentators think that US rigs have bottomed (and we tend to agree), in discussion with operators, we think the reintroduction of rigs into the market will be much slower than people expect (though it’ll certainly happen), especially given the makeup of rig drops (over a dozen dropped post-acquisition, and another handful dropped due to claimed efficiency gains).

Also quite bullishly, we welcome a part-time technical analyst to the team, which will better expand all of our offerings for both institutional subscribers, and readers of the blog. With that, over the coming months, we are going to split this platform into three distinct offerings — institutional offerings which includes model access and research offerings, the current macro coverage (what the blog has mainly consisted of, thus far), and a weekly discussion note. All subscribers will maintain access to everything. So, over the past month, we’ve worked on some great thematic research, which we will publish on a weekly schedule, and, a weekly discussion that bridges the gap between the macro discussion, and what’s happening in the equity markets. Institutional subscribers can access the model offerings through their dedicated login portals, and we will continue to build those offerings. Over the next few months, will be the schedule in which we disseminate our thematic research.

Week of August 7th: On the Permian — production declines, producer behaviours, and grading the rock and returns in a $85/bbl environment

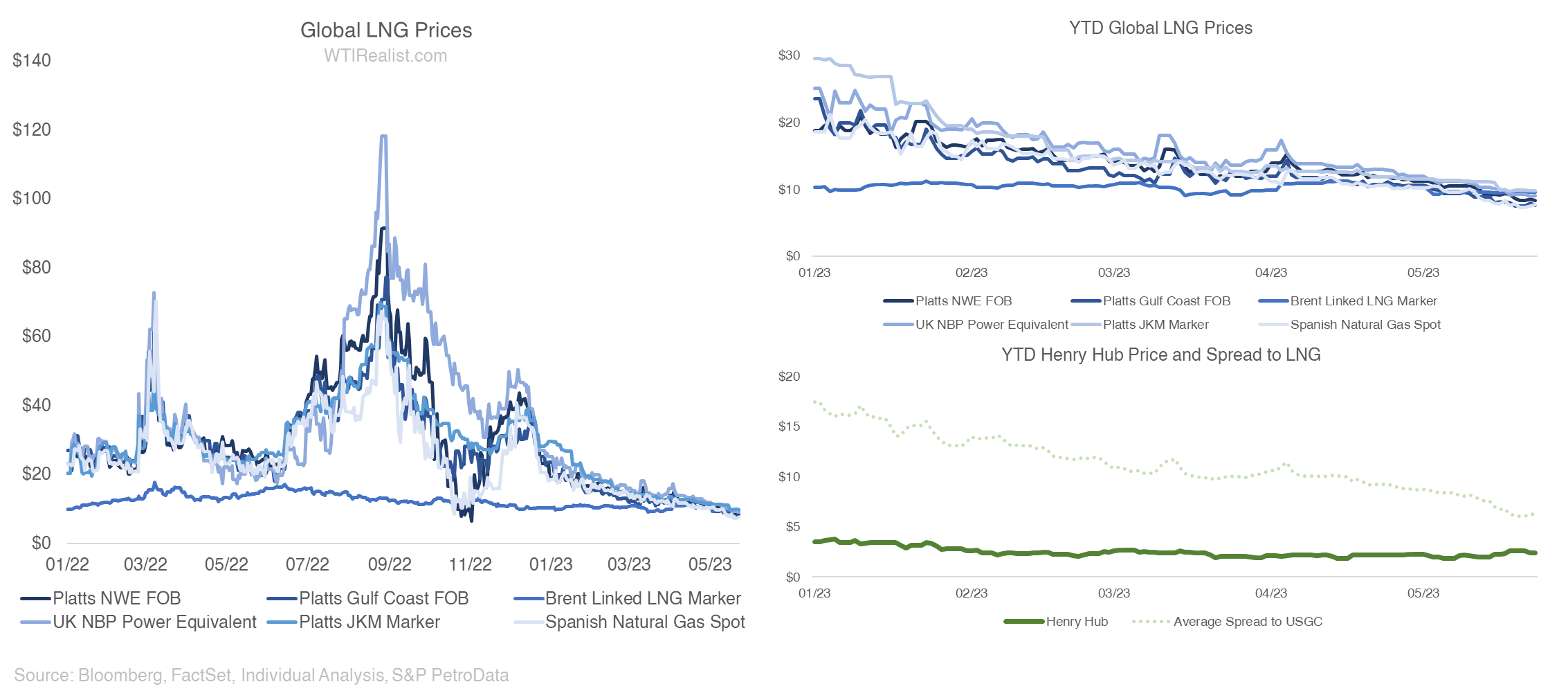

Week of August 21st: European natural gas outlook — the winter dilemma, the state of imports, and how we see the following years playing out in the LNG market

Week of August 28th: Forbidden oil pt. 2 — Russia — the long waited discussion regarding Russia’s growth opportunities, export logistics, and their oil market

Week of September 4th: The rebranded Crescent Point — our bull case for why Crescent Point, even given its storied past, may be a long into year end

Week of September 11th: “So you survived COVID” — why equities that did indeed emerge from the volatile COVID pricing environment, may still not be longs

September and October coverage will slanted towards equity coverage, E&P factor differentiation, and how we see the Alberta gas market. going forward.

For now, a list of our long ideas (note: that all equities mentioned below are owned directly, or beneficially by one or more contributors) that we maintain into the second half are as follows: