Window Dressing, or Good Business?

Window Dressing, or Good Business?

ExxonMobil and Pioneer would make sense, from Exxon's perspective.

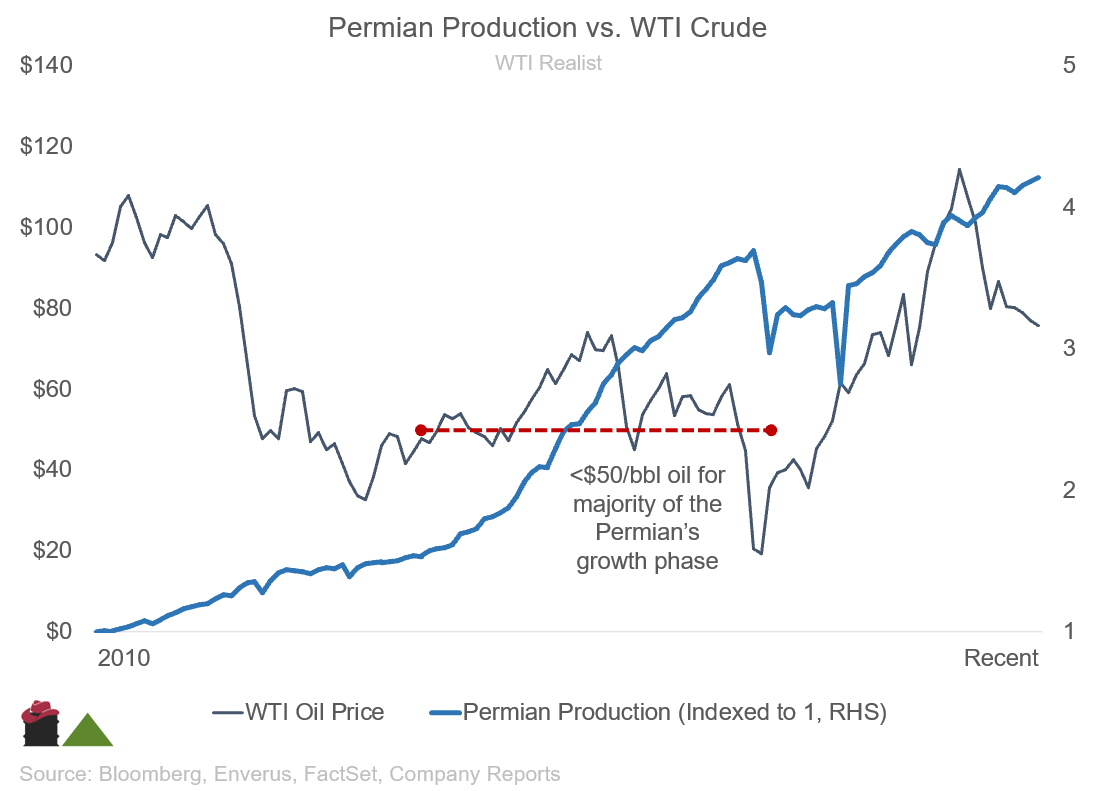

We have heard the cries of “peak Permian” for years — and I can already hear the Permian bears and overzealous oil bulls cracking their knuckles ready to Tweet “Exxon is considering more Permian because they want to cover up the high declines of their existing production, and degrading inventory quality” — yeah, that’s usually what inventory does when you use the good stuff, it gets worse, and surprise, oil wells decline. This is nothing new.

Now — have we drilled a lot of the good rock in the Permian; absolutely. Are wells high decline; you bet — but most of these attributes are well known. The Permian has been growing like wildfire for a decade, and every year operatorzs better understand how to exploit their resource. Yes, oil production falls faster than gas production as the well ages (the boe production rate doesn’t increase, the gas ratio just increases), but at that point, the wells are almost always (and in a good operators case, almost always is 99% of the time) paid off by then.

Nowadays M&A is immediately attributable to covering up high declines, or poor inventory — but what if the Permian is just a good asset to have (would that be so wild) if you can manage expectations and develop it right. In actuality the Permian is highly economic, pays back quick (though not multiple times on lower tier acreage, unlike the Clearwater which is slower to payback but pays out 3-4 times) and is well known in what it can do — after all, we’ve been growing it for a while now.

You have to be nimble in the Permian, asset returns start to sag when you aren’t drilling your wells quick (single well economics still produce strong IRRs), it’s not a defensive play, so while equity was lit on fire 2015 through 2018, even though growth was strong, returns weren't. Oil is $80/bbl today, and most land is well in the money.

Yeah, (for shareholders at least) 2015-2020 sucked — equity holders lost a lot of money, that’s just what happens when you continue to drill in an awful commodity price environment, you lose money and destroy value. But the Permian is still a good, productive, unconventional asset if you know what it can do and what its attributes are. No, the Permian is not dead, and for those that are able to acquire good inventory, pace development, and understand the geology — it can be a good cornerstone asset.

Thus, it would make sense for ExxonMobil to buy Pioneer Natural Resources.

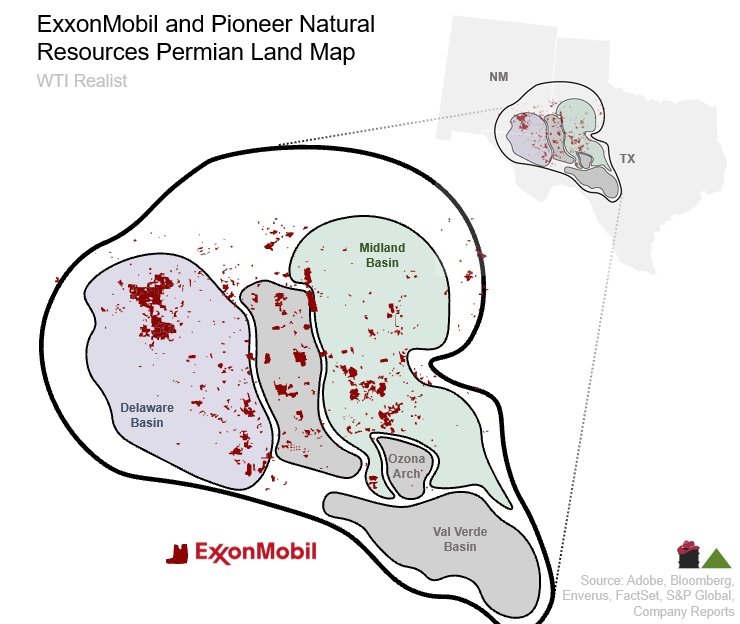

Exxon already has a great core position in the Delaware Basin, and have some presence in the Midland part, but they have a goal to hit 1mb/d in the Permian by 2027 (according to Enverus the are hanging around 600kb/d right now) — buying Pioneer would give them scale to continue to drive costs down, and it would give them flexibility on the development pace (and of course, their goal would be hit).

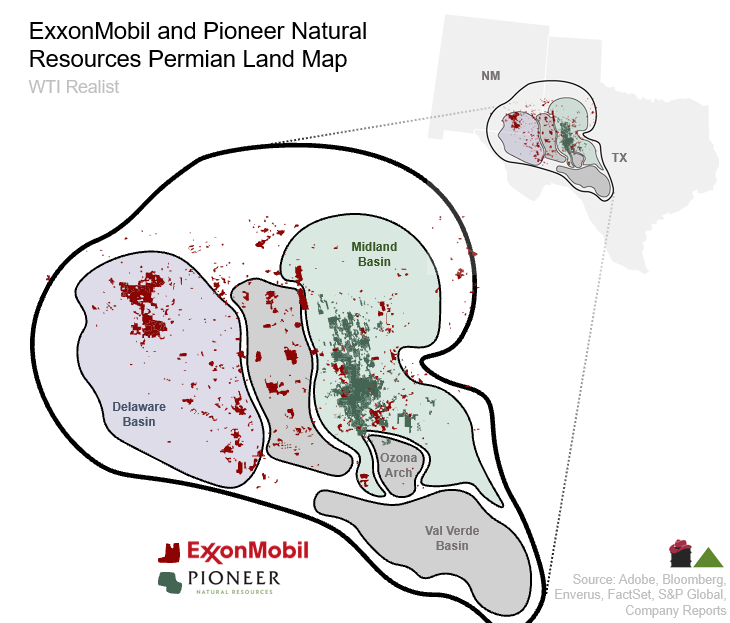

Adding Pioneer’s land position, it would make them a dominant player in the core of both sub-basins — this gives them breadth in the Midland basin. Contrary to the idea that major’s buying more land in the Permian being bullish because it means acreage degradation (and degradation means less supply and higher prices), I take it as a positive that majors are adding inventory as it allows them to continue to knock out repeatable, predictable wells for a long time while managing growth and reinvesting that cashflow into what (someday soon) will be exploration efforts — what should happen in a healthy market!

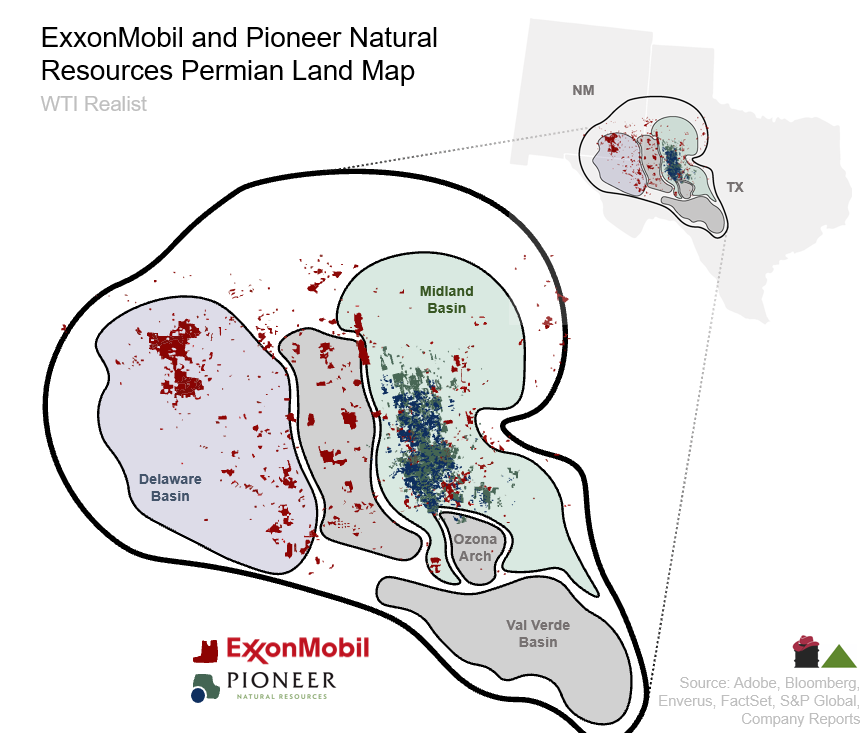

With Pioneer’s wells added as well, just to get a sense of the scale of their operation. Permian is high decline, but it’s also high payback and semi-flexible (easy to scale in and out of while bolting on production at pretty well half-cycle economics) which would make sense given that nobody is really sure where the economy goes. If a recession pushes oil down, though multiples recover exiting a recession, exploration becomes a thing again — and this gives them a stronger cashflow base to fund that. It makes less sense for them to buy something in Guyana (like Frontera) given their existing position there, and a (valid) apprehension to sink huge capital into a project that isn’t spitting free cashflow on day one.

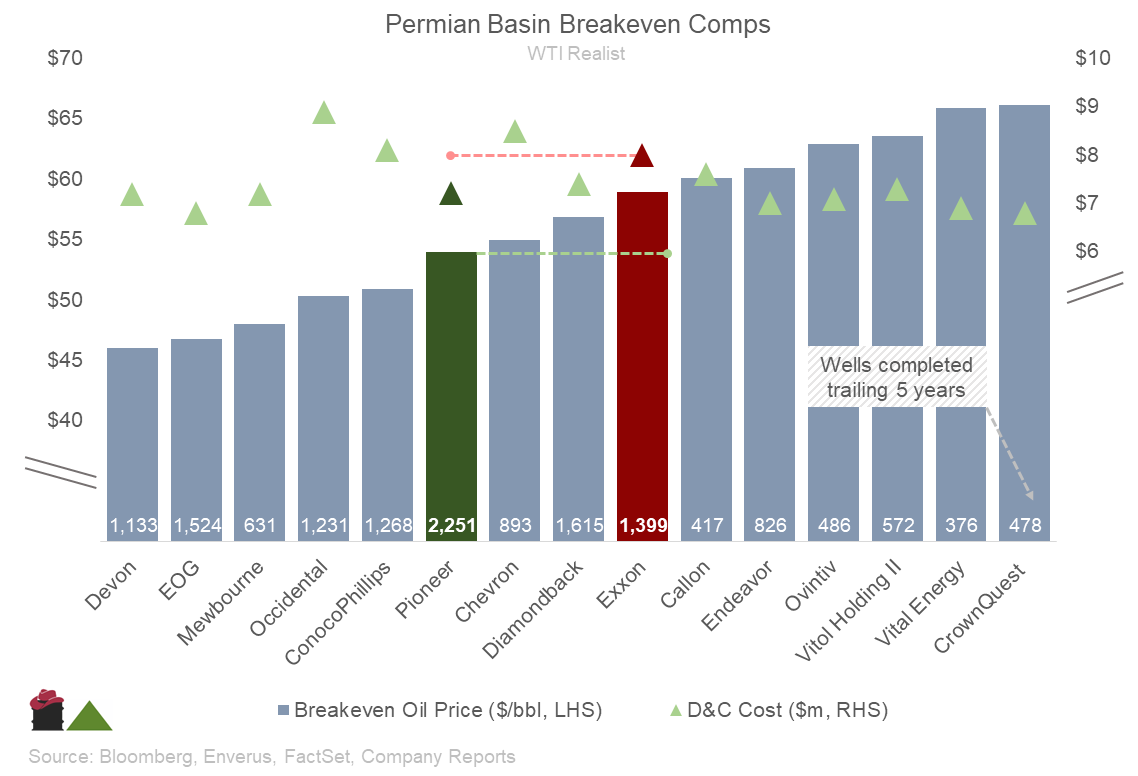

It would be accretive on a breakeven basis, as well — Pioneer has some of the lowest drilling costs in the basin (attracting and keeping good talent is going to be very important this cycle). Exxon is also incredibly experienced from their operations west in the Delaware basin. At current pace Pioneer drills around 500 wells a year (15,000+ marketed locations management says, this is ±30 years of inventory) while Exxon is running a around a dozen rigs (long term goal) and a half dozen spreads. Exxon (like everyone else) has noted crew and rig tightness, so absorbing Pioneer gives them some slack in that regard. Exxon is also very committed to free cashflow margins (10% full cycle returns down to $35/bbl is their goal, though we can debate how reasonable that is) and Pioneer’s inventory would fit nicely. It also means that a number of mid-tier companies are off that list. This leaves them with Occidental, Diamondback, Pioneer, EOG, and Devon in the public ring (in the Permian). Occidental has the chemicals segment which Exxon is likely not too eager about (and won’t sell Permian standalone), EOG and Devon are both too diversified to be appealing, which leaves FANG and PXD.

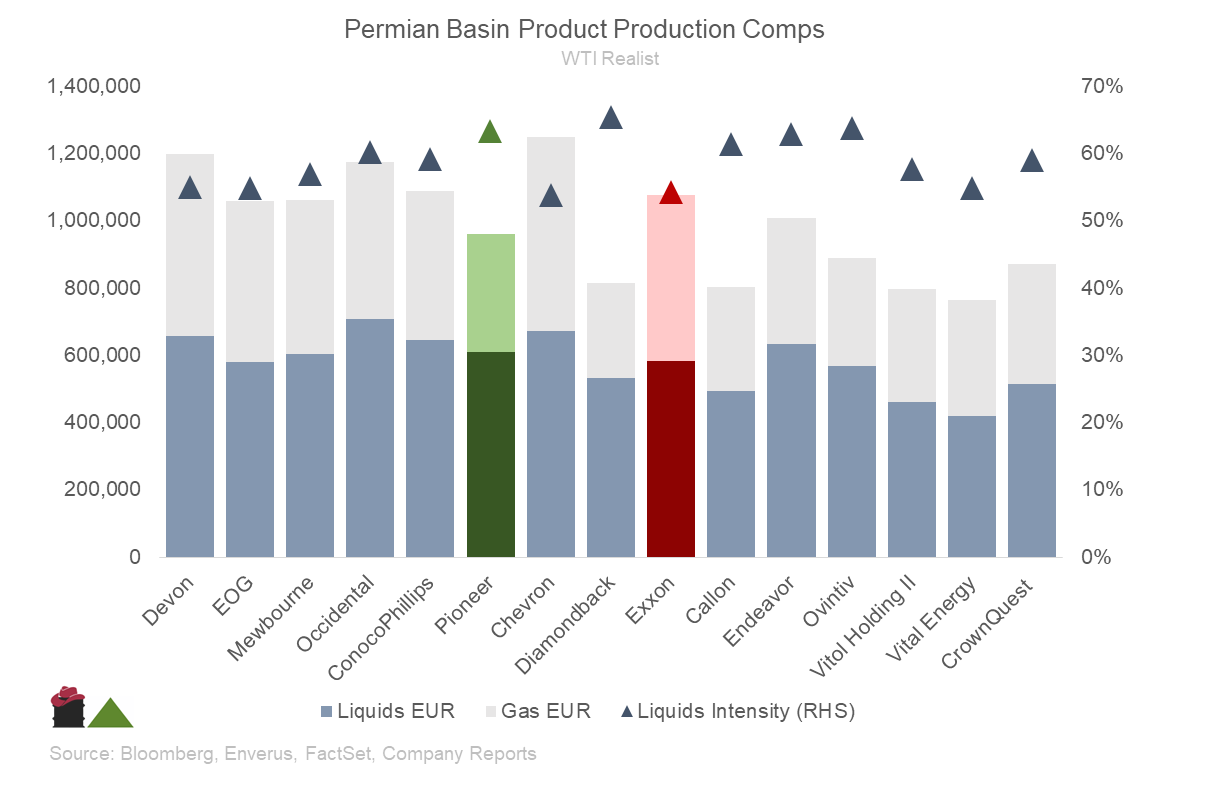

Pioneer’s wells produce less on a barrel equivalent basis, but ultimately recover more oil than Exxon’s wells. Pioneer’s IP-rates have also been softer in recent years, perhaps there is an opportunity there for Exxon. They have been working on technology to recover more and more resource, so there is room for Exxon to drill slightly better wells than we’ve seen from Pioneer over the past few years.

The remaining 2/3 of this article is for founding and paid members. Please take advantage of the promotional offer below should you wish to support my publication.