What is Whitecap?

I honestly think Whitecap is misunderstood. Its current form, and where it’s going don’t exactly reconcile at first glance, and thus it gets placed in a bucket with other mostly oil-weighted producers, and middle of the road dividend payors. But it’s more than a 5% yield and 64% liquids, it’s a bet on Grant, and the team, to deliver something great inside the next decade, and shareholders looking to the short term flags like slight type-curve beats, or small dividend increases, end up missing the forest for the trees. It’s not a dividend name, and it’s not a single well bet, more abstractly — it’s one of, if not the only Canadian SMID on the market that has a real chance at crossing solidly into that ‘large cap’ territory, and competing with Tourmaline.

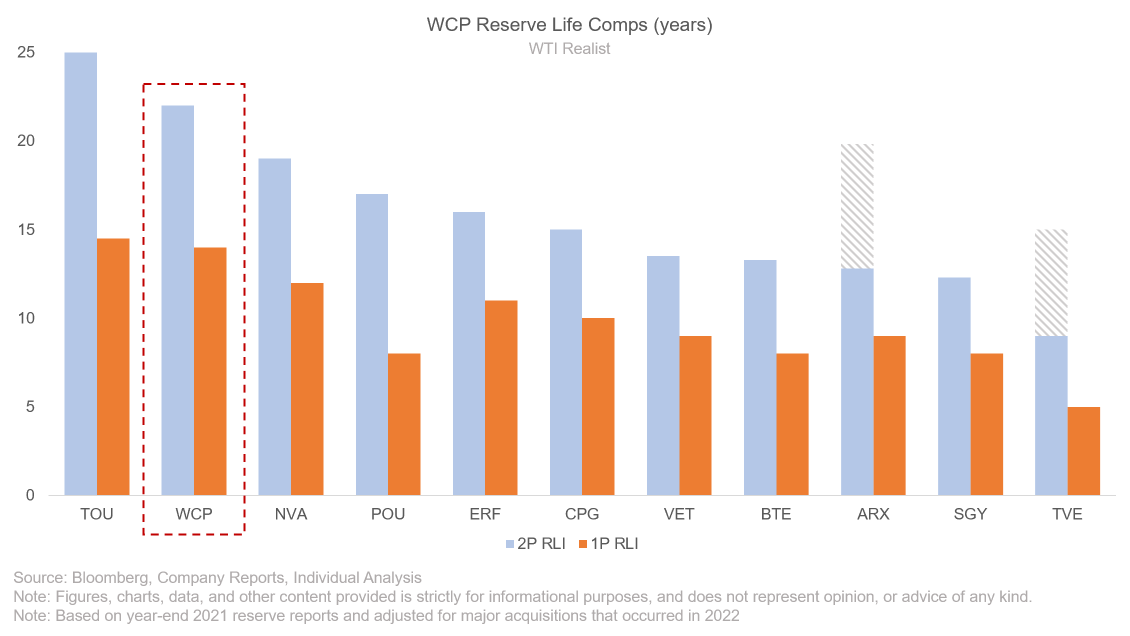

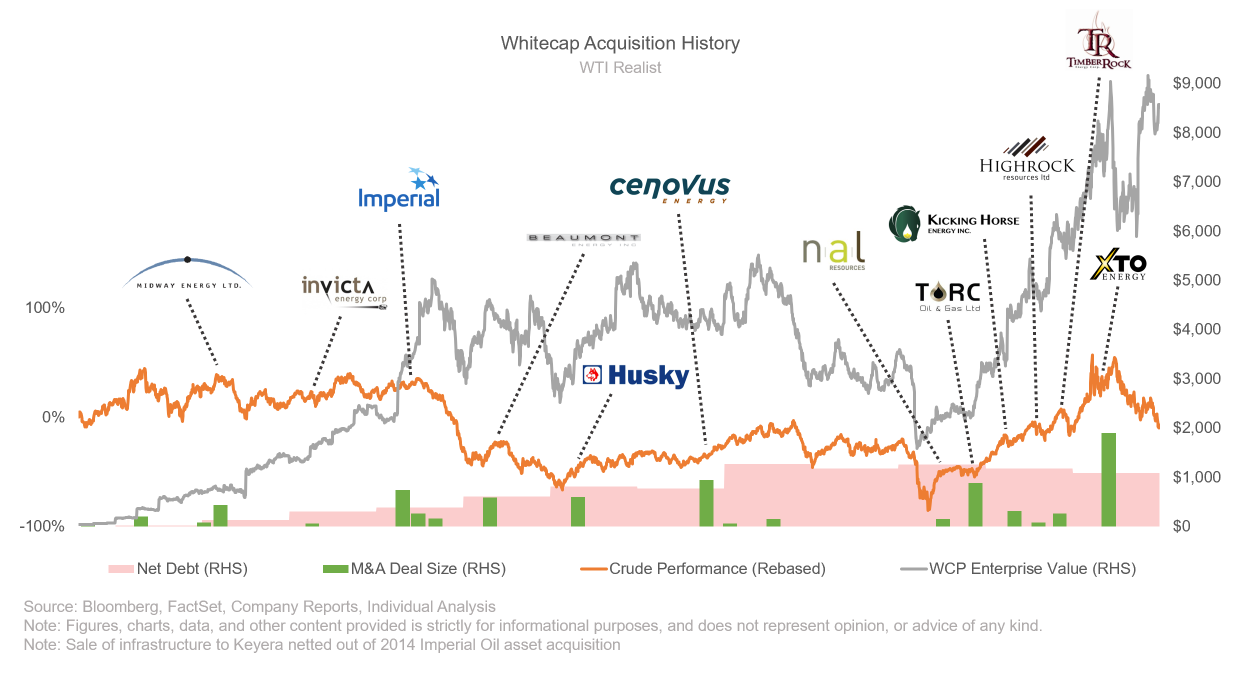

The fact is, Whitecap is one of the longest duration liquids-weighted conventional names in Canada and their recent acquisitions (think back to NAL, Torc, and more recently XTO Canada) have have given them the runway and cushioning to comfortably grow organically, while waiting for opportunities in the A&D market. Unlike other PDP weighted names like Journey, and Surge which are (for the most part) operating, and incrementally improving legacy assets (less capital intensive both on a remaining cycle/life, and acquisition basis), Whitecap has a vast land base they will continue to exploit. Post-XTO, their RLI is one of the best among peers, as shown below. They have built themselves a very good jumping-off platform.

Whitecap also doesn’t get enough credit for their acquisition history (at least by retail). They have deployed approximately $3b counter-cyclically (where the commodity price is below $60) and have made their dollar-weighted average acquisition around $70 WTI. This is a very excellent record.

It’s not talked about enough the capital they have deployed since the downturn in 2015 (and how quickly they vacuumed up value during COVID). While peers were disposing assets, they were buying.

They now have the land and skill to enjoy their long runway. They have set themselves up nicely. Not to discount small milestones and tiny wins — what are large successes but a summation of tiny wins (and small wins give us something to look forward to) — but perhaps people miss the 2026-2030+ story for Whitecap, in favour of looking forward to IP rates beating expectation — insignificant milestones on a long horizon.

Next year Whitecap will spend $70m on Kakwa development, including water build out, and their third party associated gas plants sit around 60% utilization, while their operated infrastructure hovers around 70% full. This complements their land positioning excellently, really, it’s a great setup.

On a timeline basis, it’s my opinion that most people think out 2-3 years with Whitecap (and frankly, many other names) while totally discounting, or ignoring what the goal, and eventual outcome is (a much larger business that has compounded over the years). Some names you should absolutely underwrite a half-dozen value destruction scenarios given management track record of generally doing stupid things. Whitecap is the opposite.

Think back, three, five, even ten years — it’s highly unlikely anyone remembers the exact 15% type curve beats from Tourmaline, CNRL, NuVista, or ARC. So it begs the question, why, if you believe in the company over the next decade (and if you don’t, why allocate into a name built for exactly that) are allocators focusing on the catalysts over the next few quarters. Whitecap isn’t built for quarterly beats like some other names lighter on inventory (where the amount of cash generated in the NTM noticeably affects an equity IRR%), it’s built more like a compounder, a “set it and forget it” name. The obsession with the short term is baffling to me.

See below… “slides that nobody remembers”, why should a similar slide from Whitecap then matter on a 10-year horizon?

If you’re not investing on a 5+ year horizon, why are you investing in Whitecap? There are names that are better suited to expressing a view on higher commodity prices, though the terminal value is much lower. If you’re not trying to capture that terminal value, why Whitecap?

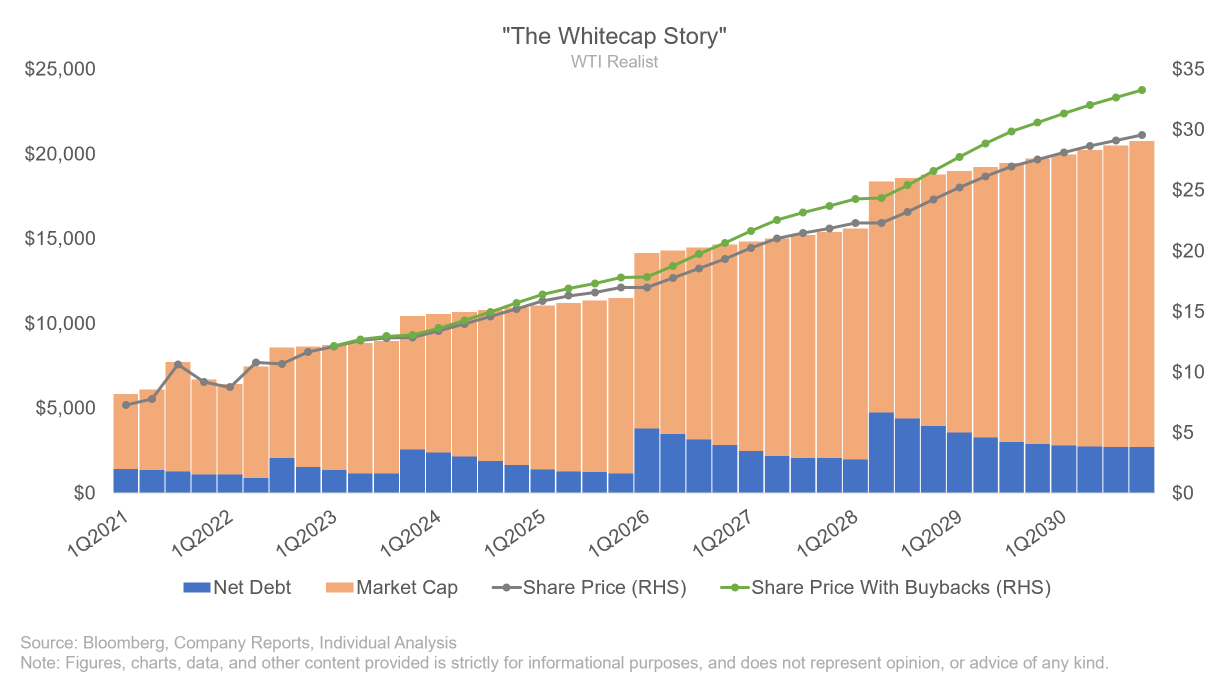

The Whitecap story looks less like what’s happening in the next few months (though reaffirms a directional thesis), and like below — the responsible use of debt to grow production and cashflows. The compounding effect of share buybacks, and the incremental improvements of capital efficiencies/synergies from potential acquisitions. All this, paired with a cap size and multiple rerate, makes Whitecap the perfect “zoom-out” stock.

There are opportunities that you miss when you think you can put an 8x FCF multiple on the LTM figure, and walk away. It’s not that easy. You ignore terminal value wether positive or negative, don’t account for management, asset quality, repeatability, or optionality — all very important in an E&P. While an 8x LTM FCF multiple might say your Whitecap upside is limited, understanding the story would tell you the opposite. It’s not a “get rich quick” resource exposure stock, much moreso, a “get rich slow” one.

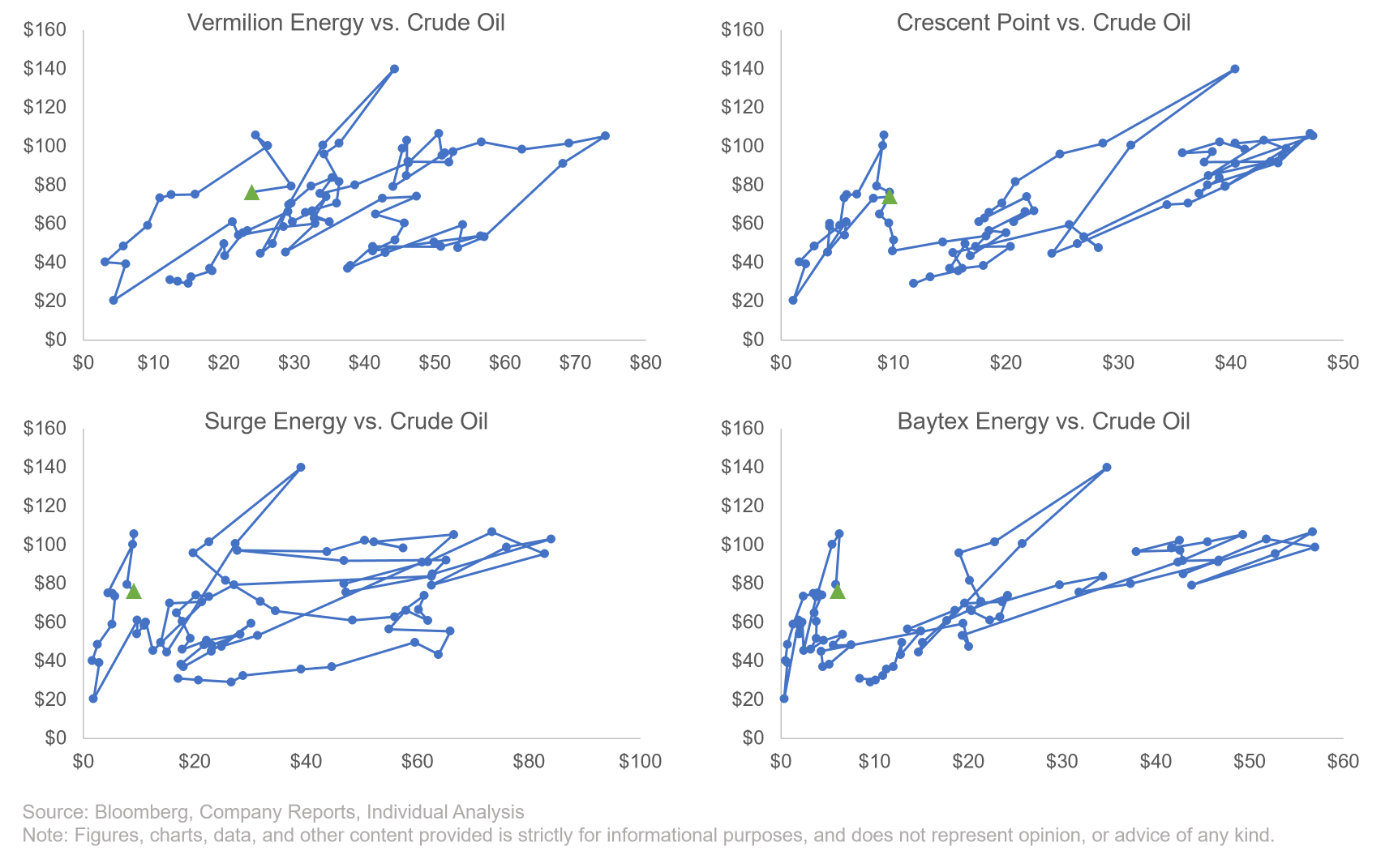

E&Ps are correlated with the price of oil, especially intermediates. Larger operations have the ability to drive value through scale, and in down markets enjoy pricing power to improve margins (to offset declines in commodity prices). While smaller E&Ps don’t have the same cost control or discipline that large-caps do.

Below is a plot of various SMID names against the price of WTI Crude Oil. There is a pretty clear correlation that higher commodity prices translate directly to higher share prices. If you follow the path, you can see in many names, where they started to overestimate their growth ability at the top of the cycle (2013-2014), then needed to issue equity to fund growth that eventually never panned out (thus devaluing their shares). Many of these SMIDs don’t trade anything near their previous-cycle highs.

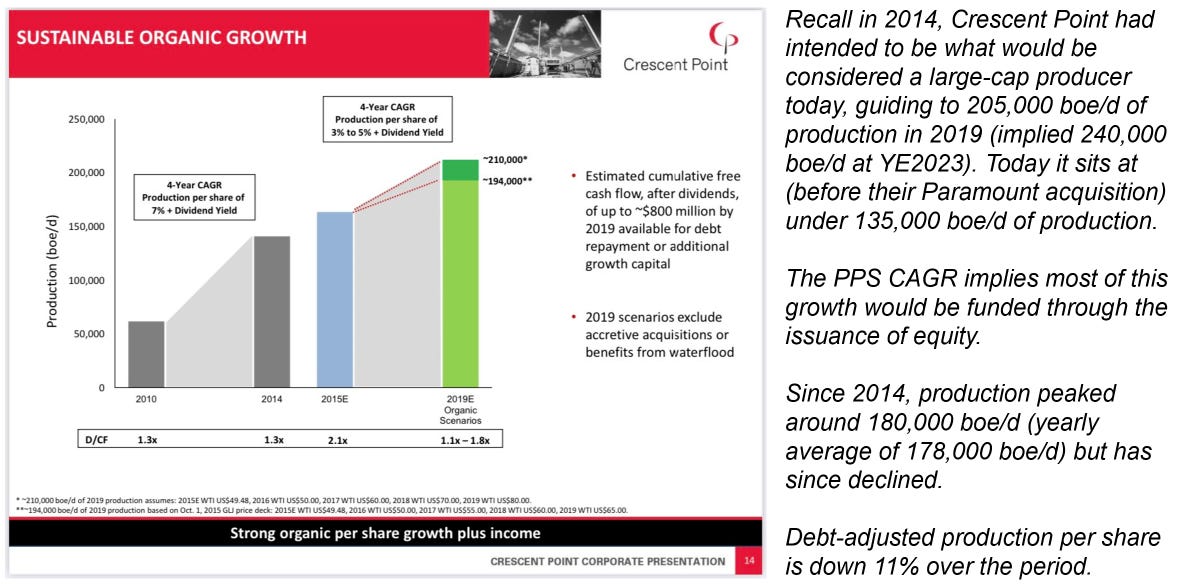

The clearest case study for this is Crescent Point which (through mostly equity financing, it’s implied) planned to grow to 240,000 boe/d in 2023, which is 100,000 boe/d higher then their current production. They were unable to successfully scale across cycles, and eventually sold a chunk of their production to shore the hurting balance sheet. This may be why, even with new management at the helm, they trade at a discounted valuation. Management is on the “scoreboard” this cycle.

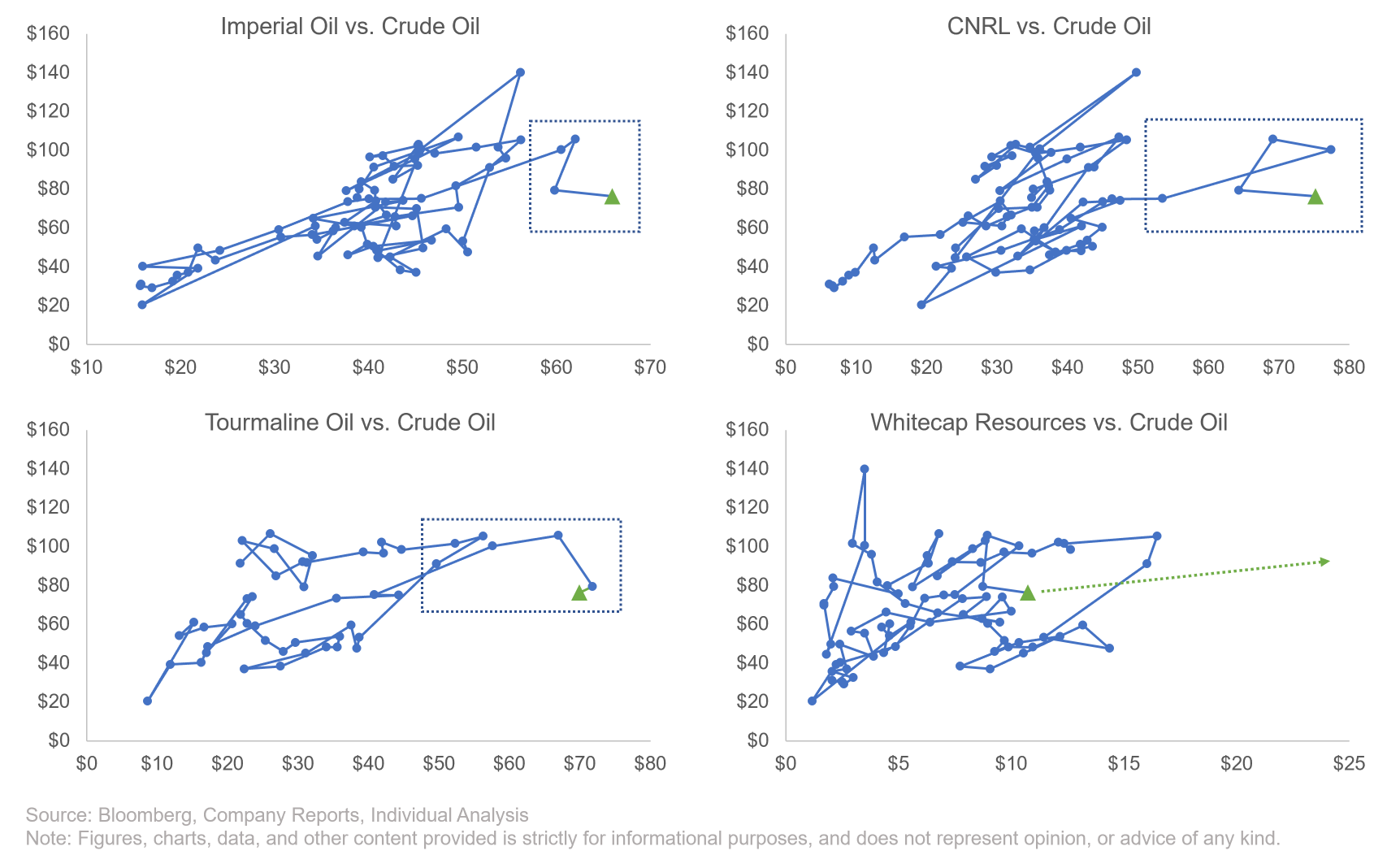

While all the names above (and the ones not listed above) also have the opportunity to create value beyond oil strip rerating, Whitecap has the best chance… “the cleanest slate”. Other peers have past issues they “need to get out from underneath”, wether it be ARO concerns, poor management performance, still too much debt, a massive float, or light inventory — Whitecap doesn’t have really any detrimental issues that plague its ability to continue growing.

Of course, a few namesake E&Ps (I’m sure you can name two of them) have managed to create value (proxy is share price increasing in a flat price environment) across cycles — that is what Whitecap is trying to do. You can see, in all the examples below, the share price slowly breaks out of that clear 45° correlation with oil prices, and eventually the share price appreciates without the lift from the commodity. This would be exactly what I see Whitecap doing if they continue on their current trajectory. This is a slow process and while small wins over time reaffirm this, they don’t majorly change their path.

So what drives the value, and why is Whitecap a contender to be one of the handful of names that have made that move right? Above all, their prudent growth of debt-adjusted production per share that really drives multi-cycle growth in share price (i.e. cashflows). If you can grow the equity’s stake in production either through adding barrels or removing debt, when commodity prices fall, you get a net levelling effect — i.e. you remove that overwhelming correlation with the commodity.

There are a few businesses that have done this over the past decade, and one that has done it so well it’s literally off the charts.