Tourmaline's California Opportunity

Tourmaline's California Opportunity

“Canadian oil and gas”, and "California” are two words you typically wouldn’t hear in the same sentence — after-all, most proponents of fossil fuels skew critical of California and their liberal energy policies, but for Tourmaline, California is quite literally the golden state. Occupying ~20% of TC Energy’s Gas Transmission NW pipeline at 2023 exit, Tourmaline will be providing ~15% of the Pacific Gas & Electric Co.’s (PG&E’s) natural gas — roughly 5% of the entire state’s natural gas demand.

The lack of local production, and pipe constrained imports, means that cash markets for natural gas in the state can get obscene, and are only exasperated by low storage or cold weather. In the dead of December 2022 a cold snap had gas selling for $60/mcf, over 10x the spot price of Henry Hub. Storage woes also contribute to the volatility in cash pricing, as there is no resource to instantly draw as a buffer when demand spikes.

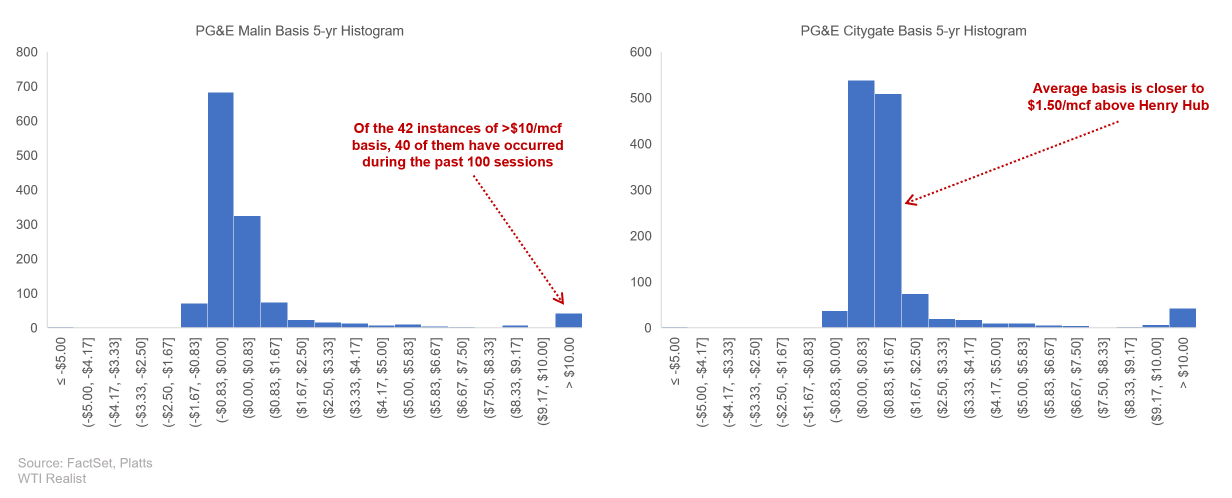

California is structurally short gas and Tourmaline is capitalizing on that weakness (or helping them with grid sustainability, one sounds more ESG). See the histogram below to truly appreciate how erratic (and favourable) the cash markets have been for Tourmaline in California. Over the past 1,300 trading sessions, only a few dozen days have see prices >$10/mcf to Henry Hub. 95% of those days were in the last year.

Having access to these markets has been incredibly lucrative, with the average realized price for the two PG&E benchmarks (Malin at the north border, and Citygate near San Francisco) being over 2x higher than Henry Hub. You tend to see higher volatility come at times of lower storage, and California’s storage is low. Pipeline maintenance, nuclear downtime, and higher (and lower) extreme temperature have left useable gas storage dangerously low. See the chart below, as storage pewters (like in 2013, and 2018) the local prices get pretty wild. Not surprisingly, the same happened last year. While national storage fills to generally the same levels year after year, for the past decade, Pacific storage (CA, OR, and WA) has been setting lower highs.

Though, $50/mcf natural gas isn’t sustainable for utility companies, consumers (insulated through utility pricing), and en masse, the local economy. PG&E has already gone bankrupt twice and is mostly unable to pass their generation costs onto the consumer (while their prior bankruptcies were not a direct result of this power cost spread, it makes quite a nice point). Hence, PG&E needs normalization in the market.

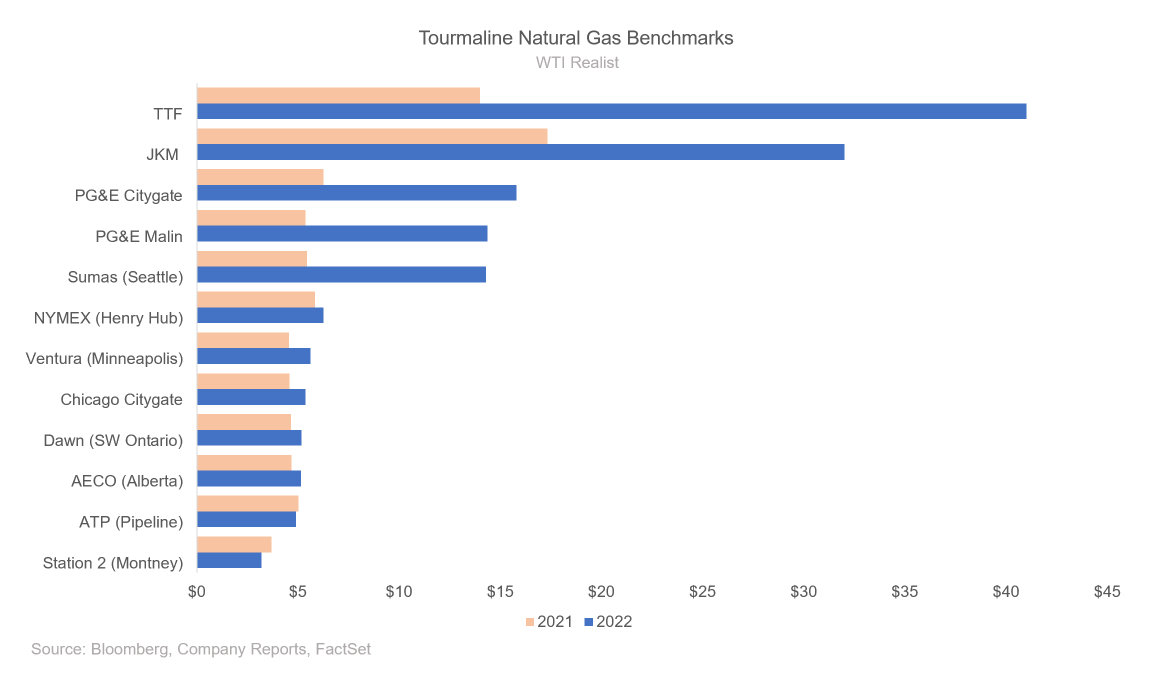

While the sale price Tourmaline gets for their gas in California isn’t straightforward (selling into spikes can boost realizations that isn’t reflected in the futures pricing), if you were to extrapolate their $15/mcf realization in 2022 into 2023, street cashflow estimates are light by a few hundred million. For reference, below are their main natural gas benchmarks (as reported in the Q4 filings).

A normalization of basis would put ~$40m of Tourmaline’s unhedged revenue at risk per quarter (for comparison’s sake, their quarterly FCF is ~$500m). With a board mandate to hedge ≤50% of production, Tourmaline has been opportune in adding production hedges (basis and swaps) while high benchmark pricing persisted in markets that are typically not high (like AECO), this has meant there has been less hedging in markets consistently receiving a premium to Henry Hub. With their financial hedges (at strip) the sting of complete normalization would be closer to $100m yearly, and strip versus 2022 realized price is in the $1/sh range (special dividend anyone).

Though the risk of California gas prices softening somewhat just got real — it rained.

Over the past few weeks, the mountain passes of California have been hammered with >100” of precipitation, in just 10 days. At the UC Berkeley Snow Laboratory, they have recorded the 3rd snowiest winter to date, with >200% the average snowfall thus far into the water year (which runs October to September the next year). The Pacific’s trade winds will sometimes do that to you.

While the rain in California would not usually be a cause for concern, especially for a Canadian gas producer, in Tourmaline’s case, it’s a direct threat to the fat gas premiums they’ve been enjoying in California. Hydroelectric power has the installed capacity to provide ~20% of California’s energy mix, but with drought like conditions in 2020 and 2021, its actual generation has been <10%. When other renewables fail, natural gas fills its spot, as a cheap (relatively), and easily deployable generation source.

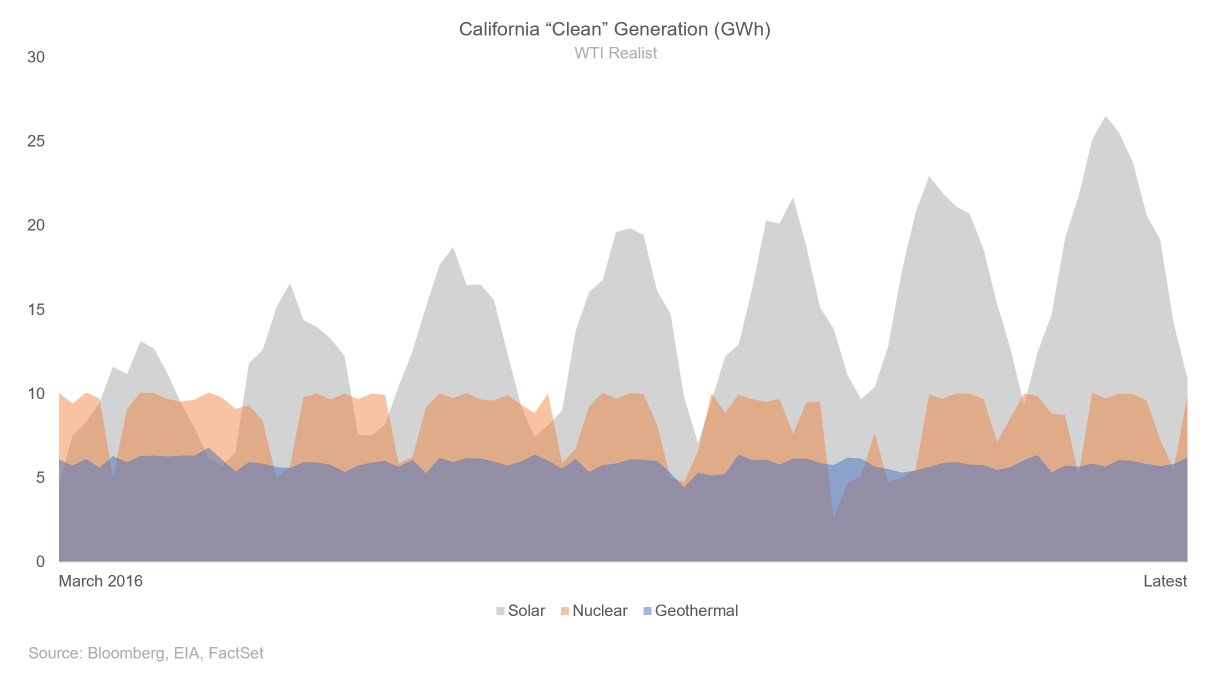

While solar is generally ablated for being intermittent, cumulative solar generation, and capacity has continued to climb in California, complemented with 10GW of consistent nuclear and geothermal capacity. It’s slightly ironic that unpredictability of solar that fossil fuel fans criticize, is the same unpredictability that is responsible for a windfall to producers that can get their gas to California. Though that’s neither here nor there (perhaps we should all become champions of solar?)

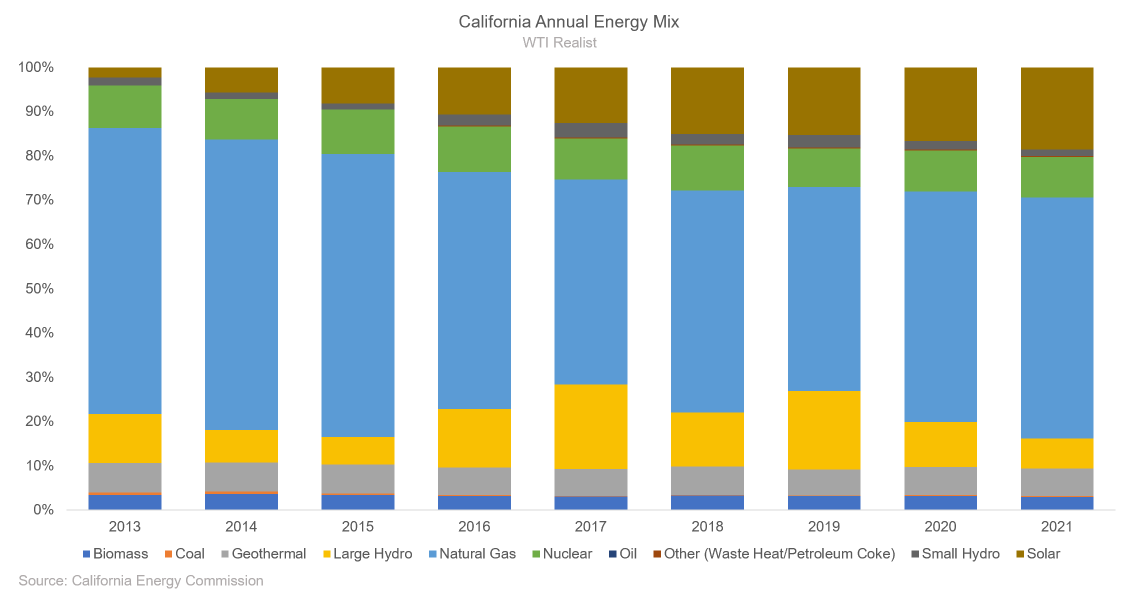

With most of the energy mix accounted for, the two variable generation sources are hydroelectric projects, and natural gas (which also doubles as peaking capacity, hence the expensive gas). Below is energy mix (relative) over the past 9 years in California. While solar’s cumulative contribution has climbed, it’s the yellow (hydro) and blue (gas) that fill the bulk of power demand. Whatever hydro can’t provide, natural gas must.

Here’s where the rain gets interesting.