The PubCo Incentive

The PubCo Incentive

Misaligned motivations destroy shareholder value

There are two distinct “ologies” in shale — at least I think. Geology, and psychology. Of course, on the geology side, you want a thick, deep reservoir, high porosity and permeability, large amounts of organic matter, high pressure reservoir with adequate natural lift — when all those factors align in harmony — you have a core play. When you start dropping characteristics, like encountering thinner pay — you start to move down in tiers — yes, surprisingly (and to the disappointment of select management teams) — there are means to accurately and repeatably classify reservoirs into different tiers — it’s not just vibes based (though a handful of operators have certainly pushed what “core” or “tier 1” means).

The other “ology” is psychology — and in the short term, something I would posit, is much more powerful than geology. When the incentive is in place for a management team to focus on short term value, and get paid, rather than long term optimization — the limits of what your reservoir can do, are quite possibly ignored; and it’s why I believe, that US production will be resilient for longer than many shale bears think. Stick with me on this one while I extol my thoughts.

Before we get into it — I’ll make some bold statements — per foot production degradation isn’t important for a while (there will be a fight) the Permian will continue to grow (albeit, not without pushback and struggle), and the infamous shale decline isn’t really a story before 2025. You might read that and laugh — what a crazy thing to say — well degradation doesn’t matter, psycho thing to write.

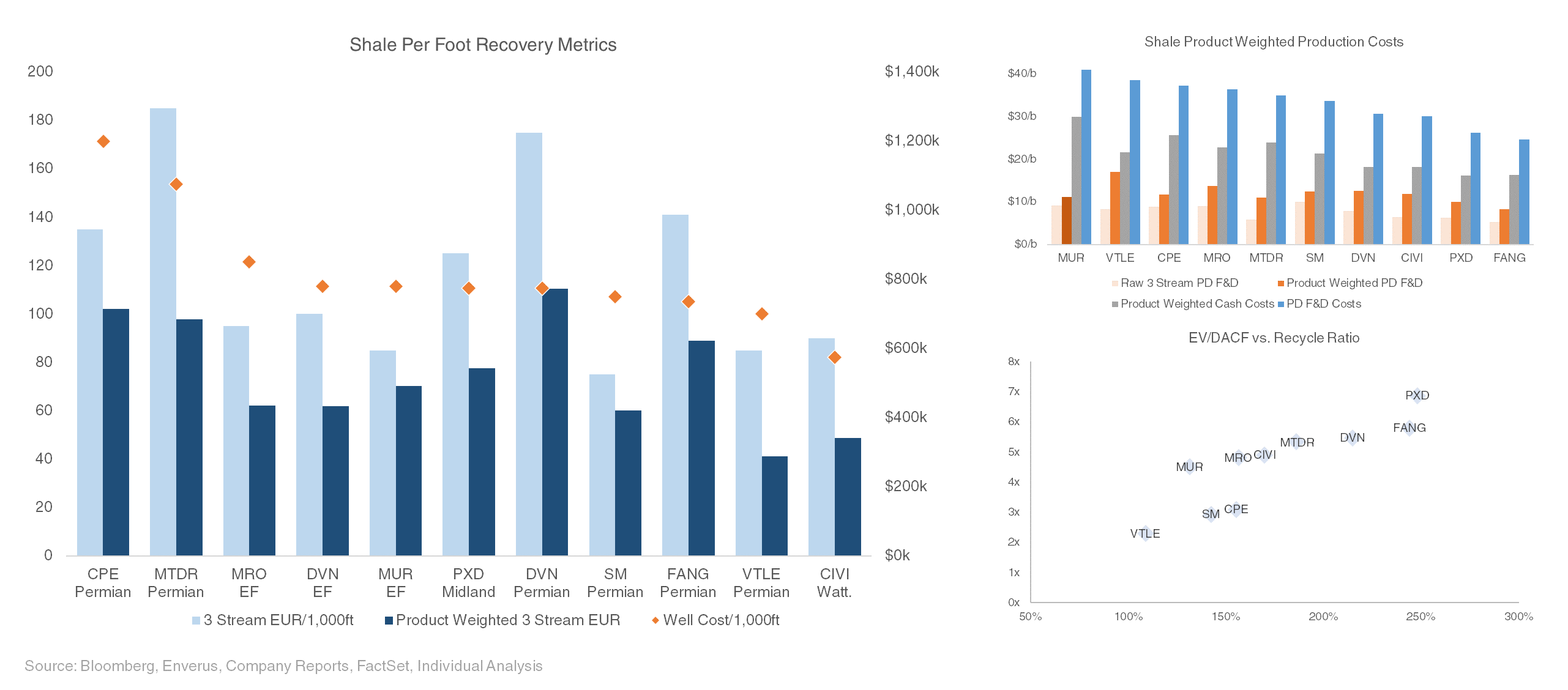

Is it? Is it really far fetched to say that shale operators will generally do stupid things that are not entirely aligned with shareholders, and likely destroy capital in the process? Totally unreasonable to think that shale operators will continue to do whatever they can do to survive after a little taste of $100/bbl? Let’s not forget that without the post-COVID and Russia price run up, lots of these things would be zeros — and wind is back in the sails, temporarily. You just need to make it to that super cycle promised land — and I think, psychologically, that is the important part that the geological focused shale narrative misses. Your inventory is so economic at $120/bbl, DCET costs can inflate at 10% a year, and you can lose 30% of your well productivity and you’re still laughing. Take Vital Energy for example — today, they have a 3 stream EUR of ~80kboe/1,000ft (around 35% oil), and a well cost of $710k/1000ft — which puts their F&D cost around $20/boe. With a $50/boe realization and $23/boe in operating costs, they are barely positive on a recycle ratio basis, and when you add in $8/boe in corporate costs — negative on a free cashflow basis. Jack that realization to $120/boe, call the well cost $950k/1000ft, and cut productivity to 60kboe/1,000ft — and on a much higher price deck you are not only extremely free cashflow positive, but your recycle ratio is well into the 200% range. For slightly-more-core operators (but still fringe), like Devon in the Eagle Ford, which sits at an asset level recycle ratio of ~1.6x right now — they can see their productivity fall 30% and costs rise 30% and their ratio would stay on side. So — the obvious thing to do right now is survive. Shale fails at $70, but shale absolutely rocks at $120 (which in of itself is kind of the problem with the bull case that revolves around shale failing driving prices up, because higher prices really give shale operators a huge margin for error). If you’re running a $40/bbl PD F&D business — you absolutely need higher prices, but (discussed later) — if you start to deliver earnings misses, you start to spiral your stock downwards (which is detrimental to the value of all those share units you’ve been granted over the years).

Generally though, management incentive is kind of skewed to hit targets at all costs — because that’s how you get paid. See the charts below — on the left you have the amount of cash salary available through a non-equity incentive plan, and expected volume growth this year. Obviously, if you’re not getting paid for growth, no chance you’re going to grow this year (it’s not right) — but, if you are getting paid for it — pedal to the metal. Same story on the right, where you have total excess compensation at risk (including share and options grants, and bonus) versus the change in return on capital from 2015/16 through 2019. Those that don’t get paid to care — don’t. Bottom right shows the change in the business capital intensity (growth is worse, and defined as capital employed divided by barrels per day produced), and again, the names that just get paid to produce barrels at any cost — produce barrels at any cost, for little regard to the underlying health of the business — and I think that business degradation theme is going to play out big time in the next few years of limbo, where names become continually reliant on some sort of price turn, and you don’t want to own those — so here is what to look for.

The remainder of this post is for paid subscribers, should you wish to subscribe, please follow the link below. Note — on June 1st, the price for new subscribers will increase to $55/month, or $500/year.

I am pleased to have added enterprise access to OilChem high frequency granular Chinese demand, refinery, and supply data which will significantly upgrade China crude and product coverage, the most important part of the crude story.

I have also added additional S&P Platts access, frac spread intelligence, live vessel tracking data — to improve the quality and breadth of my publishings, something I continually aim to do.

Existing subscribers will continue paying their current subscription price.