The Path Higher, or Lower?

The Path Higher, or Lower?

How different really is it this time

If you truly want to be an energy specialist, you have to think like a generalist. It’s a weird statement, but if you don’t truly assume (mentally) the role of an incremental buyer, the pretty charts with free cashflow yield differentiation between tickers means sweet nothing, and flopping in and out of names with no outside capital flows is more akin to Ralph Wolf and Sam Sheepdog clocking in and out every day.

Where instead of Sam and Ralph showing up to the sheep’s pasture every morning, exchanging pleasant chit chat then proceeding to chase each other while Ralph attempts to abduct sheep — we sit down at our desks, wait for the 9:30am bell, and bat the proverbial tetherball that is energy equities back and forth from broker to broker, dealer to dealer, savaging other market participants for a few pennies, while we tell ourselves we are “up-tiering our book” — only to meet at Earls afterwards for drinks.

We’re all so specialized within the sector — engineers could talk for days about just a single part or apparatus, bankers can tell you about the 5 basis points they grinded out to get a raise done, geologists could name every formation in every basin without skipping a beat — but what we don’t really do is reflect on where energy fits in with the rest of the financial world. Yes, we circlejerk and say nobody can live without energy, but don’t really consider, sometimes that makes a bad investment. We can’t live without airplanes, cars, utilities, hell, a lot of things — but all those sectors are also notoriously tough businesses. Just because “energy is life” doesn’t mean people need to own the equities.

For now, we’re the marginal buyers (yes, energy enthusiasts that already own a lot of energy), and unfortunately for us, the prices at which we are willing to keep buying, are a lot lower. We will tell ourselves “it’s too cheap, super cycle incoming” and keep buying all the way down, all while actual marginal capital (institutions, family offices) flock to other sectors, while we reaffirm our physical market biases with nice graphs from Vortexa and Kpler, ignoring the capital markets reality. See, the issue is, the current marginal buyer, is a buyer at a price much lower than today, and we are going to, in my opinion, continue to test that price lower as sentiment continues to decay. While funds flow out of the sector, it’s people that already own energy, simply averaging down. For the whole, y’know, supply and demand thing to take effect, and markets to bid energy back up, you need a shift in sentiment, and big time.

Our biggest flaw, as energy specialists, is thinking that energy is our comp group — it’s not. As noted before, on Twitter, and in my Vermilion yearly look-ahead, as energy folks, our comp group is not energy companies, it’s high free cashflow yield, low debt, well run businesses, that exist in every sector — and the harsh reality for us, is that most of the other companies that fit that bill, don’t have an overwhelming terminal value risk, government regulation risk, environmental risk, are likely less immune to sentiment changes, and less immune to recessionary forces — we don’t really fare too well. See, the thing we kind of have to wrap our heads around, is that, besides energy specialists, the incremental buyer for energy right now, are focused funds, typically underwriting to 20-40% annual returns for LPs, and they aren’t interested in “getting paid to wait”, they are interested in catalyst driven, short term situations where they can make 20-30% in a few month timespan, and exit. Energy no longer offers that, especially going into a recession (or whatever you want to call it). So, our marginal buyer group — people that want to lock up chunky positions in SMID cap names, is practically nil — and therein lies the issue. Energy doesn’t really present an asymmetric opportunity anymore for most buyers.

When it comes to the physical market, I hate to tell the reader — the physical market can be strong, and the equities be weak. It’s all sentiment driven. Talking heads can appear on TV and say that “we’re looking for a booming 2H23 recovery in demand, with up to 2mb/d of undersupply”, but none of that matters, none of it. What it means, is that companies may see multiple compression, and trade flat in price, as capital continues to sell in expectation of a significant market event (read: recession). Until you can thoroughly cleanse the idea of a recession from the veins of the market, it’s my opinion that your energy flows are going to continue to be destitute. The physical market can continue to tighten, and equities can continue to trade flat. I think that is something that needs to be repeated, re-read, and maybe even embroidered into a throw pillow and given to every single energy long on earth — energy can always get cheaper — and it tends to get really cheap into a recession.

The kicker — most recessions have some sort of oil tail event that triggers the obvious ‘recessionary’ vibes — what does this mean — the more expensive oil gets (all the bulls want), the fewer and fewer people want to buy energy (on account of confirmation of a recession). It’s a sticky situation to be in. It’s the harsh reality, and I would suggest everyone read this piece with an open mind.

AUM between the large energy ETFs in North America has generally been resilient, but, with the banking crisis (that yes, does indeed matter a whole lot for your energy holdings), flows out of energy have been huge, and quick. The last 1Q OPEC+ cut announcement temporarily brought about some excitement, but since then, we’ve stagnated, and that is not a good sign.

Around $3bn has flown out of these ETFs, with outflows weighted more towards the exploration focused ETF (XOP) than the general energy funds (XLE and XEG) — suggesting that even within energy, people are selling down risk, I don’t take this as a generally bullish sign. If we are seeing risk sell, we’ve just seen the first leg of flows out of the energy sector, if general economic conditions start to (or continue to, I’m not even sure) worsen, the broader sector ETFs likely start to crumble.

Adjusting the AUM for flows, well, it’s not really a great look here either, in the XLE, we have 35% to the downside before we revert to our pre-COVID average — wether that comes from people selling down energy holdings, or AUM grinding lower, I’m not sure, but there is slack for selling pressure to continue.

Of course, you could look at the above chart different, and read the general flatness, as new sticky capital within the energy sector, that is likely to stay and restrict outflows. How you want to read it, up to you, me personally, I don’t see it as overly bullish.

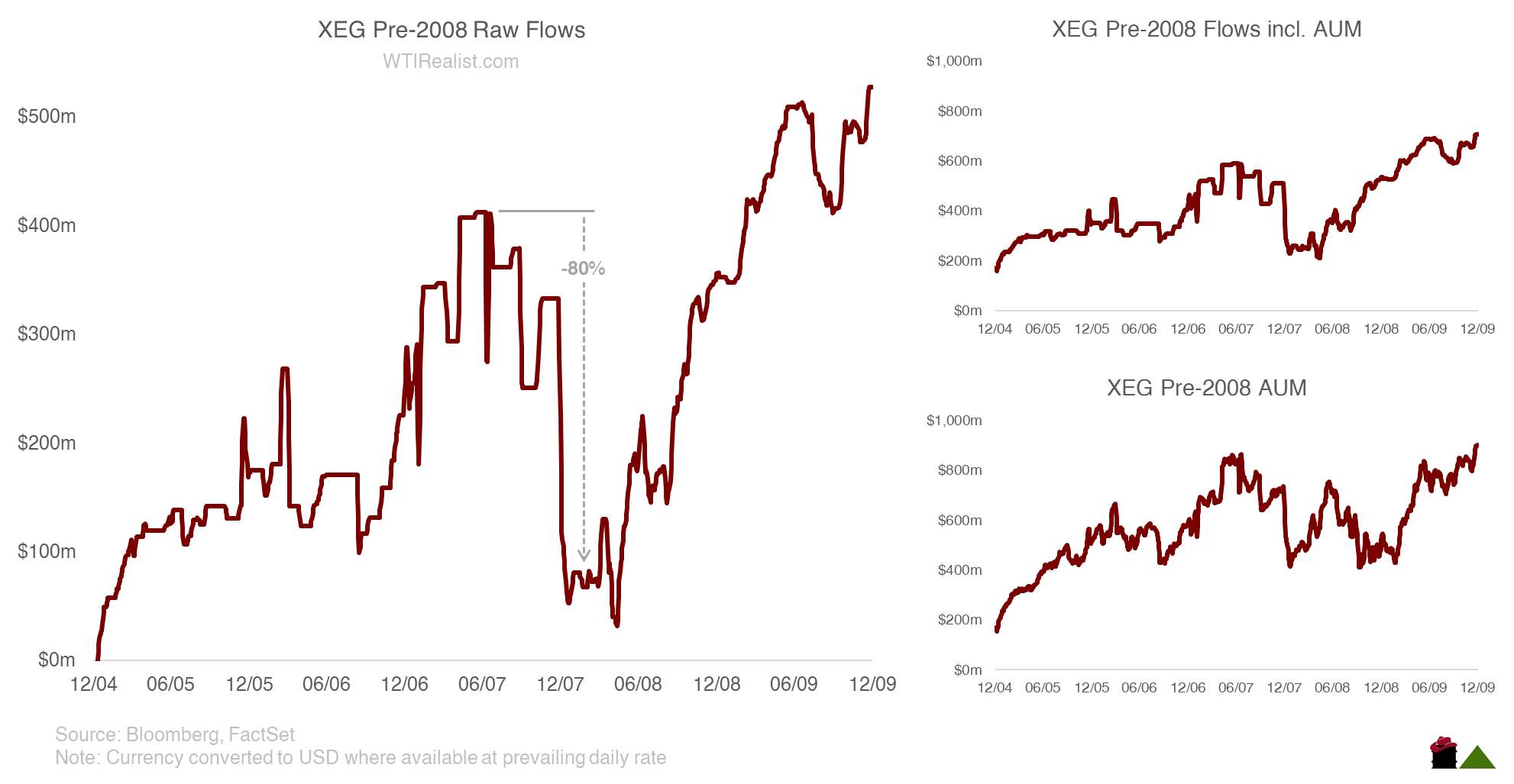

Though, we need some historical context to really pair with, to understand what happens when there is some tail event — so below are XEG flows during the 2008 financial crisis. Unlikely to be the same magnitude today (as the ETF was also, much smaller back then), owners derisked heavily before the financial crisis, with AUM halving from 2007 to 2008, and almost 80% of the previous inflows being rugged from the ETF — not really a good sight on the funds flow side into a recession.

Though, that’s enough talk about flows, because while it lays the premise for the rest of the post, it’s really more ‘vibey’ than it is data based (we can argue all day about how much money comes in or out, though we won’t know until it’s historic data).

The more important discussion — what happens to energy equities into a recession, or into some sort of unexpected event? Well, the answer is “they probably get cheaper”. Yeah, not what you want to hear, but lets discuss.

Heading into 2008, even as oil was indeed ripping, multiples compressed by around 1/3rd, and into mid-2008, equity prices were flat. Some may then argue that the multiple floor is around 4x DACF (8x-ish FCF), though I’d disagree — since the last major recession, E&Ps have burned a decade and a half of inventory, costs have increased significantly, and overall, most have been kind of useless at creating value. I’d be more inclined to measure multiple drawdown than absolute multiple, and at ~25% drawdown right now, I think you could see SMID multiples settle as low as 3-3.5x DACF, which would imply something like another 20% of downside, broadly, across the SMID universe.

While stocks generally get marginally more expensive as oil prices increase, when you are fighting a recession, the trend reverses, and equities start to get cheaper the higher prices go — for the whole recession confirmation idea discussed above, and the obvious implied demand destruction, but less obvious factors, like credit tightening (and E&Ps are still reasonably levered) and cashflow uncertainty tend to increase volatility which has knock on effects through the trading behaviour and capital structure — it’s tougher to be an E&P in a volatile price environment with an uncertain future, people tend to pay less for companies like that.

Which is the main issue with the argument that demand can increase into a recession — yes, that may be true, but along with that, is sentiment that is rapidly deteriorating, and if sentiment is low, equities don’t go up — plain and simple.

Thank you for your readership. If you have not already, please considered adding yourself to my mailing list, or becoming a paid subscriber to gain access to private articles, models, and other content. The remaining 75% of this article is for paid subscribers — please take advantage of the promotion below should you wish to support my work.