The Chinese Diesel Red Herring

The Chinese Diesel Red Herring

Are things really getting bad in the east?

On Saturday evening, Bloomberg reported on rapidly building Chinese diesel inventories, and as much as I’d have liked the immediate opportunity to jump all over what could be inferred as declining gasoil demand into a slowing economy — we’re all about being realistic here, so I took a pause, let the brain idle for a few hours, and while it’s not overtly bullish, I think there’s a good argument to be made as to why it’s not cause for immediate concern.

Recall March’s OPEC+ note, where softer-than-expected Chinese demand growth is likely the resolve between an undersupplied, and a balanced market, thus — it’s crucial to get China right going into the back half of the year, and our chance of getting China right is exponentially lower if the approach is one-sided. We have already established that China GDP estimates definitely have room to come down — we are still at a broker consensus 7.3% y/y 2Q23 real GDP print (though the 2Q22 print saw serious deceleration, so less fretful) and a FY23 y/y real growth estimate of 5.3% — with context, China grew 6.2% y/y at the lowest of the GFC (1Q09), though before COVID, their rate of growth was slowing, posting a 6% y/y print in 2Q19. China GDP estimates are definitely not conservative, but that’s something we knew. Combined with this distillate inventory build, and reported declines in industrial trucking activity — it’s key to understand if this diesel inventory a true leading indicator, or just more noise?

Like most flags the market has given us over the past 2 years — there is a strong case to be made that this is simply global balances shifting/rearranging themselves; and for the most part, the underlying thesis is directionally unchanged.

Unsurprisingly — Russia is to blame.

It’s general theory that Russia postponed maintenance on refineries as sanctions came into affect (while managing supply chains) leading to local inventory builds through the end of 2022 — which is part of the reason why exports have been persistently high (inventories drawing to backfill) while production has been reported as softening. Now, as inventories in Russia begin to normalize, exports have been ramping (as we now have the tanker capacity to move products) — this (should be) a short lived phenomenon, also partially owing to the EU’s embargo on Russian refined products encouraging as much buying activity from soon-to-be-sanctioned parties. So — the amount of gasoil for purchase on the open market is up markedly over a few months ago — while demand is (in this scenario) unchanged — so makes sense then that eastern inventories build (where typically east of Suez would buy crude and sell it back west, that is temporarily, not the case).

This works out to be a truly epic rearranging of product routes (i.e. the market) — where crude tankers are earning the same regardless of size, when normally, larger carriers should cost more (which is less on a per barrel on board basis).

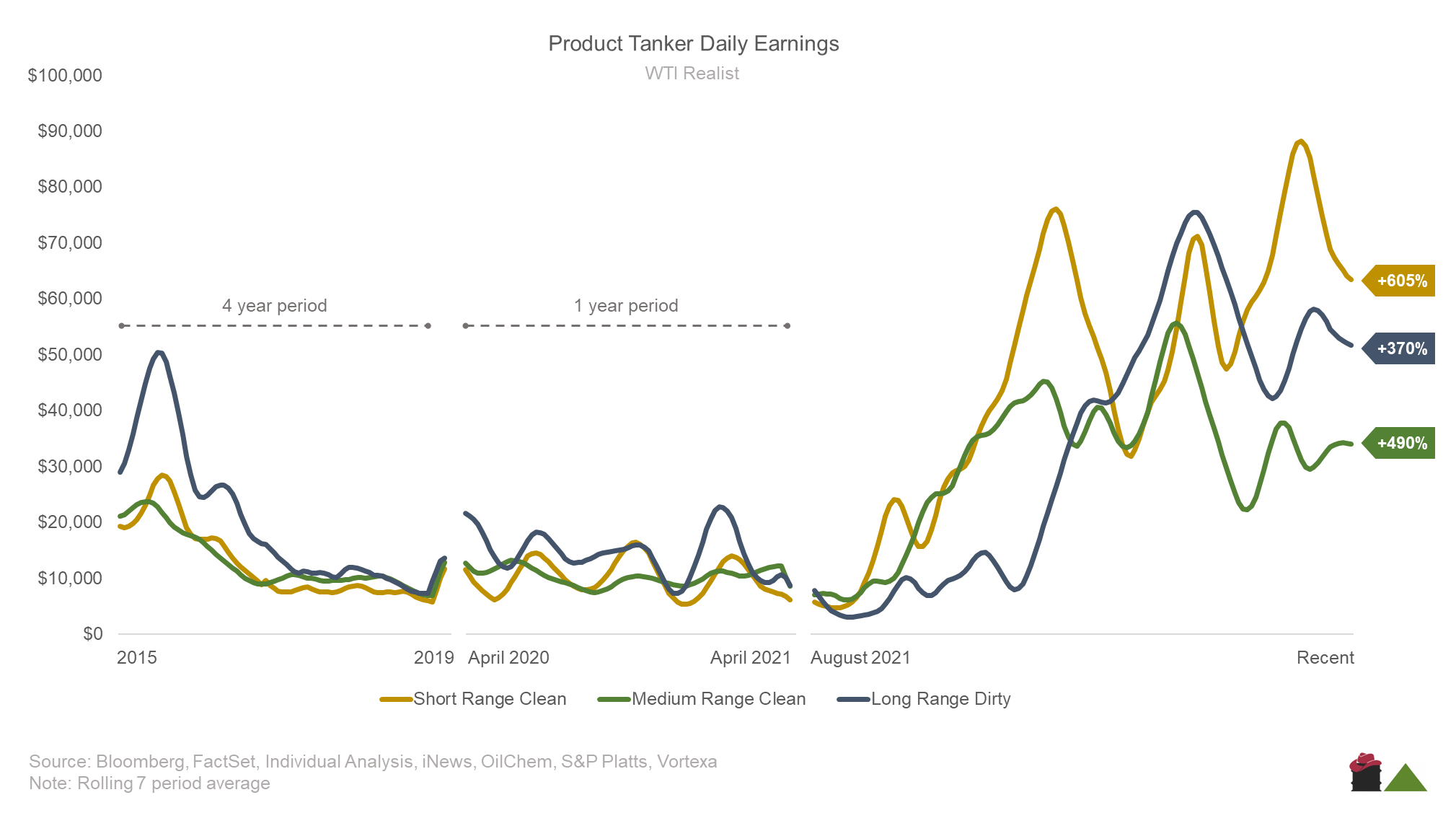

The same size story is shockingly visible in product tanker earnings — where more maneuverable Handysize vessels (that carry ~300kb compared to ~450kb on a Panamax, and 900kb on a Suezmax) are significantly outearning both long range dirty tankers, and medium range clean tankers, and on percent increase over 1H21 average, short and medium range clean tanker earnings are outperforming long range dirty tankers, which fits with the market reorganization thesis.

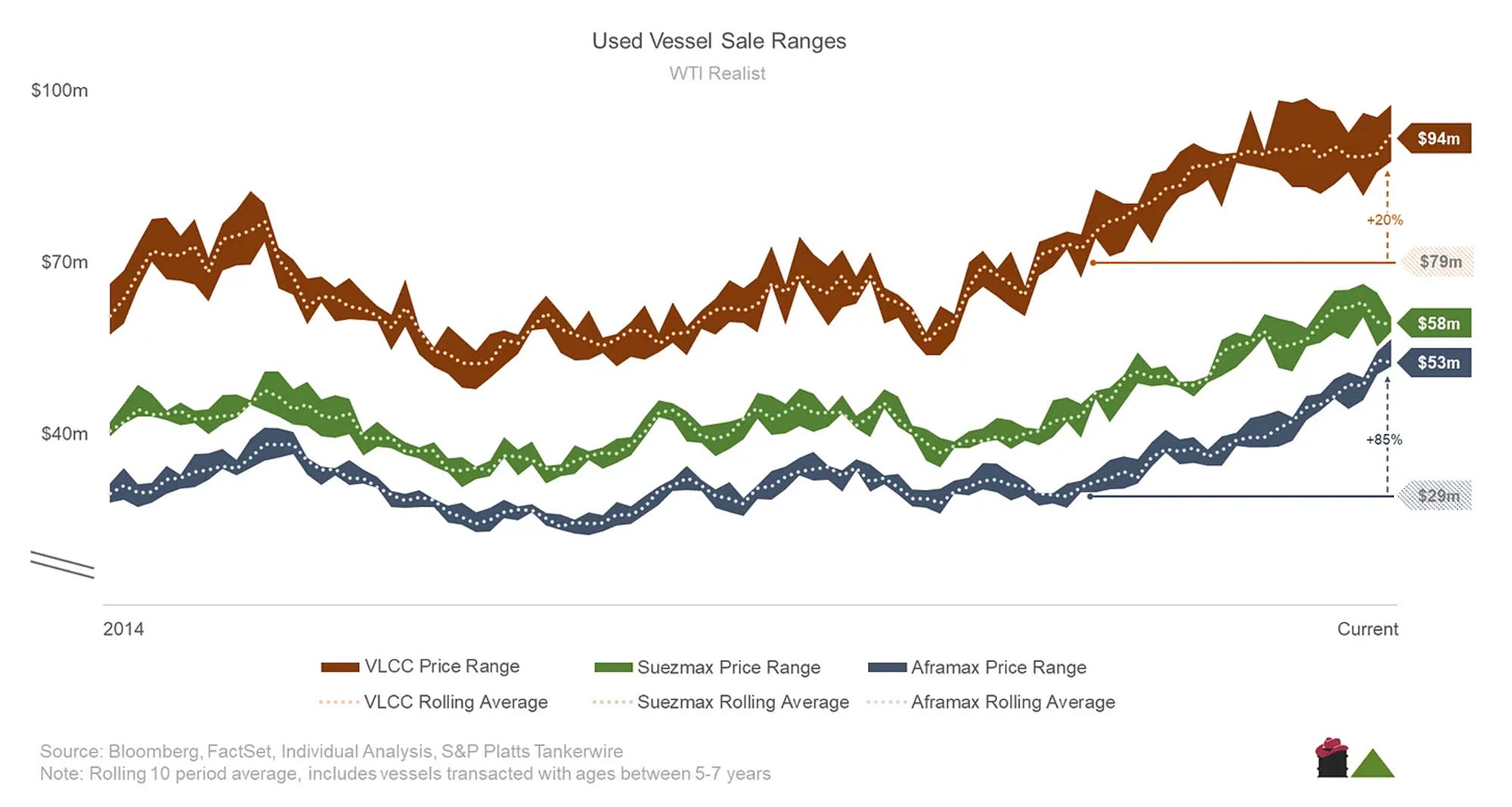

New build prices are still in check, especially so after adjusting for the price of raw steel — which helps reinforce the idea that the demand for medium range vessels is (at least by market participants) likely to be a short to medium-term phenomenon. Used bulker prices have also softened into the new year, while used tankers have climbed significantly higher; the fact that used vessel demand is only in the tanker segment (again) suggests that the market is finally settling into its post-Ukraine invasion normal — given that >50% of Russian exports are petroleum products, compared to ~20% wheat, metals, etc. (i.e. bulker demand) — the short term spike in used tanker demand ties through.

The opposite pricing surge is true for used vessels, where Aframax vessels are up 80% from two years prior, while VLCCs are only up some 20%. The demand for medium range vessels (and the activity of medium range vessels from Primorsk and Novorossiysk) only confirms the idea that we are rearranging the traditional Russian product flow routes.

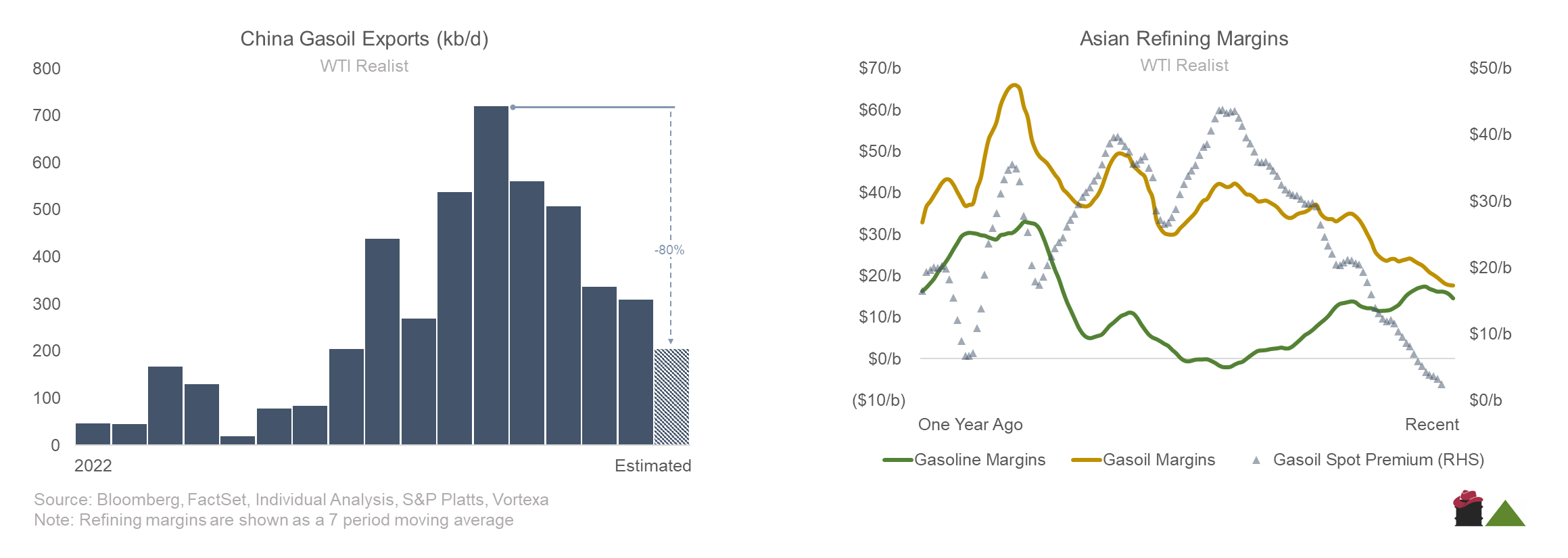

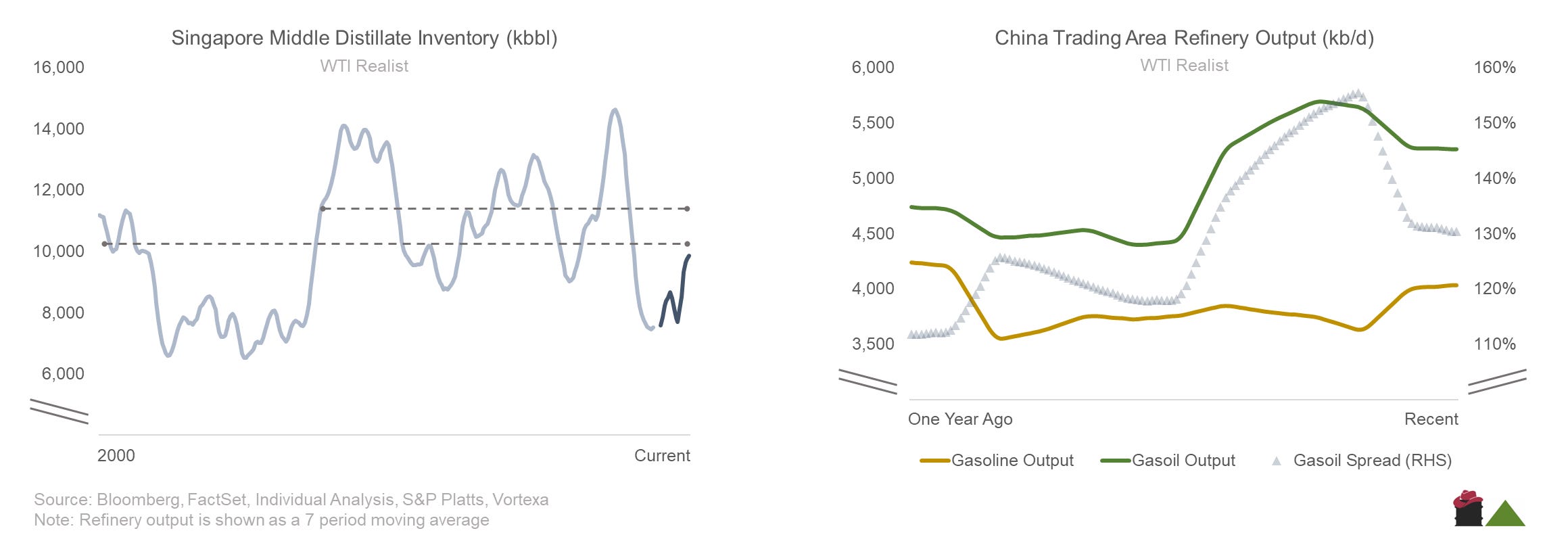

So — back to Asia — the China distillate story starts with Asian refiners chasing diesel cracks thanks to cheap ESPO feedstock, and increased global diesel demand (and softening global middle distillate inventories). This meant significantly higher Chinese gasoil exports through the end of 2022 (when inventories were drawing).

Since then inventories have built (which is seasonally expected as well) as gasoil margins have come in significantly, and focus switches to lighter products like gasoline. China is already reducing gasoil exports/production (and the trend is expected to continue), so the inventory balance situation should moderate shortly.

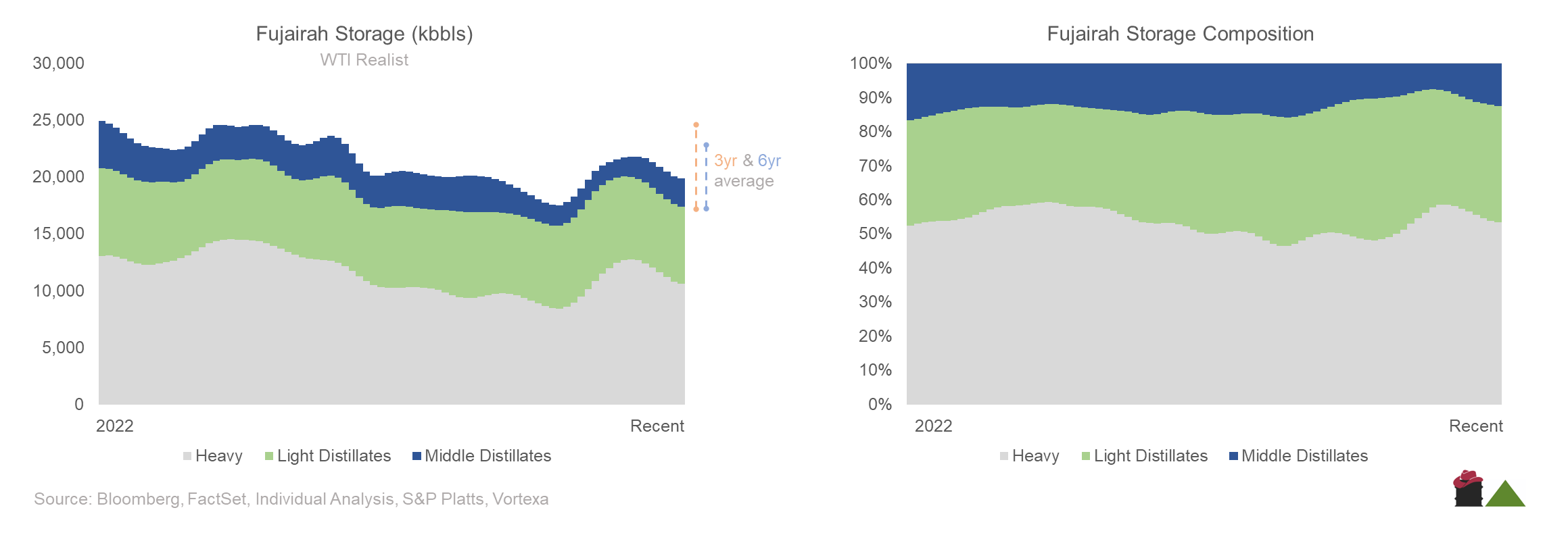

The west still generally needs gasoil, Fujairah (Dubai) middle distillate storage is below seasonal and longer term averages, which should pull some of the inventory from Singapore and China, and once the surge in Russian exports works its way through the market/inventories, we should get a better idea of true demand levels, and where gasoil cargoes need to end up.

Right now gasoil is being stored in Asia (Singapore inventories below) while tankers chase other work (and Russia pushes exports hard). South Korean, Japanese, and Chinese refiners are already lightening their gasoil output in favour of gasoline.

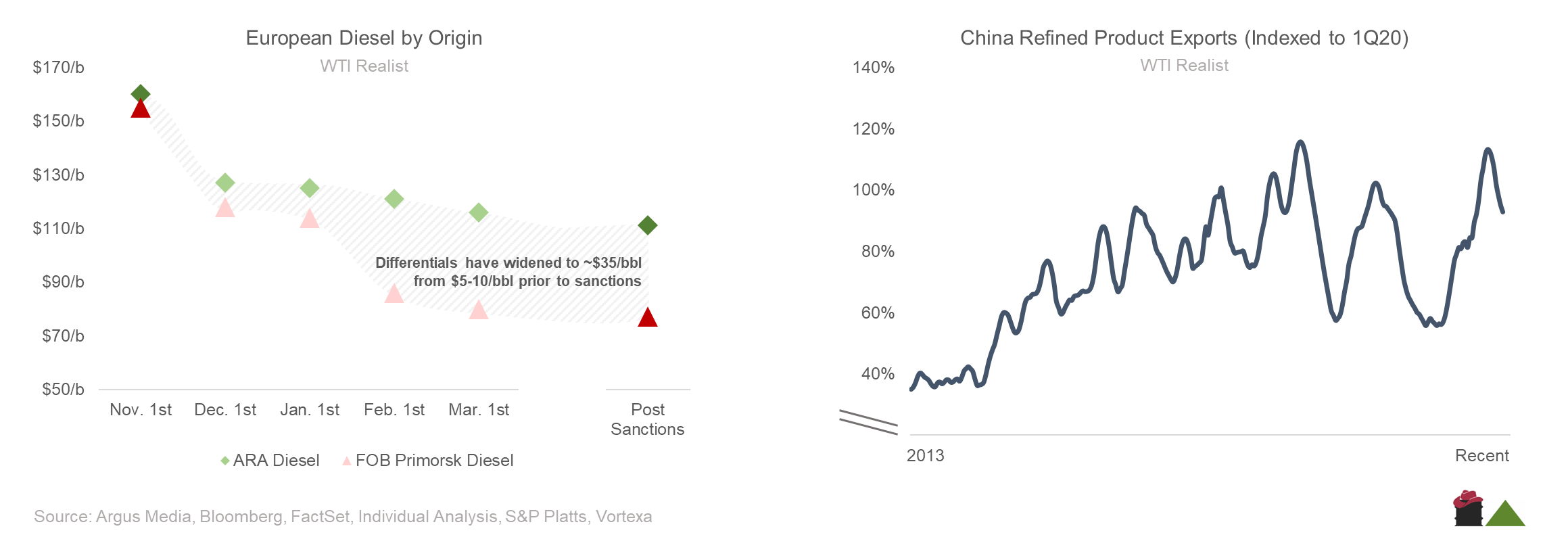

While Chinese exports start to roll over slightly (suggesting more local demand coupled with moderating export prices), European diesel benchmarks remain persistently high and Russian diesel remains widely discounted. For now, Russian diesel should make it’s way into inventories throughout the world, and Chinese exports should continue to work their way back to equilibrium (slightly higher than currently in my view) with normalized international import capacity, and the slow ramp in local Chinese demand through the summer. Right now global import capacity is backed up with the surge in Russian exports, and Chinese demand is still recovering. Net those two out and we are on the cusp of a healthy balance.

With Russia working out its logistics chain — you start to see products from them make their way to the Mediterranean, Africa, and Asia, instead of Europe and the US. In the Mediterranean vessels are generally idling ‘FOB destination’ before transferring its cargo to another tanker once a buyer is found. It’s tricky to insure Russian cargo (and tricky to buy it), so this is becoming a popular workaround where countries can still use Russia as a crutch without admitting to purchasing their exports. It’s the same story with Africa, where tankers head for the Western coast (think Togo, Ghana, Nigeria) to transfer their cargo before heading to their final destination (typically South and Central America, or around the Cape of Good Hope to India, or East African hubs like Sofala/Beira or Mombasa).