The Cadence of E&P Multiples

How valuations have, and may evolve

The E&P you own today, is going to be different than the one you own when you actually you want to own E&Ps (during that famed impending rerate). That’s a bit of a loaded statement so I should rephrase — the E&P you own today, is going to be different than the one you own when you actually you want to own E&Ps.

Wait, that’s the same statement (see what I did there) — yeah, it is, because as David Bowie said — ch-ch-ch-ch-changes. You’re about to ‘face the strange’. Let’s break it down. This morning I’m going to focus mainly on SMID cap names — as that’s for the most part where people tend to hang out, due to differentiation, and more ability to create specific exposure to certain plays, markets, and management strategies (the bigger you get the more scope you inevitably pick up).

The very issue that the bull thesis builds their foundation on (no investment), is resolved with lower free cashflow. Not lower free cashflow in the sense that prices fall, instead, lower free cashflow in the way that exploration and capital spend increase — because that’s really how you create value in this business (not just distribute it). We can argue all day about buybacks, dividends, acquisitions, divestitures — but without continued strong reinvestment on the micro level you aren’t doing yourself any favours. The advocates for what is essentially PDP blowdown models are not your friends — they want cash from the business, quick. On a full cycle basis (I say this a lot, and really, it means looking at all implicit and explicit costs of a decision for the life of an asset), it is less productive to take reinvestment to the bare minimum — it hurts the assets, your returns, and while the tourist may be happy, making decisions to appease shareholders really isn’t much of a winning strategy as a public company.

Unfortunately — when you take away free cashflow, you lose a lot of your captive investor audience, and that 15-20% free cashflow yield no longer becomes an appropriate comparable (because capital in excess of maintenance is creating tangible value, something you the shareholder reap) — which is one of the (to be discussed ad nauseam later) flaws of this whole “previous cycle multiple” idea.

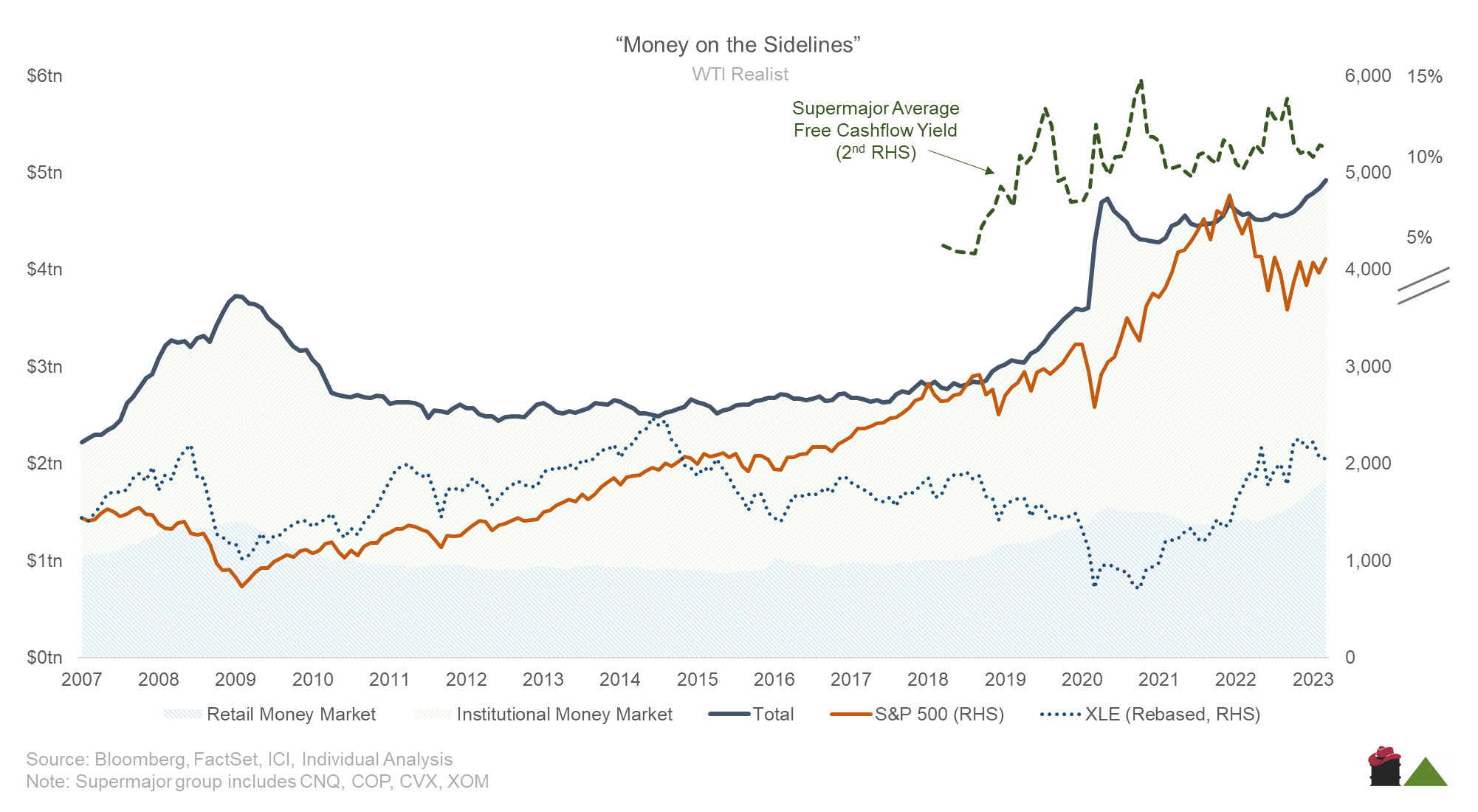

The market doesn’t buy the durability of energy — and that’s one of the main reasons we haven’t see the across-the-board bid we all wake up every morning hoping for. Wether it’s recession fears, or just aversion to the sector, money managers and retail market participants have been keeping their spare cash in money market instruments instead of high-yield supermarjors (which would for all intents, be considered safe). Even when money market accounts were paying sub-1%, energy still saw outflows.

If there was a time for that ‘sideline money’ to bid into energy equities it was when COP was yielding 10% and the inflation theme was just starting to play (and a recession quite hadn’t dominated the headlines — yet). No dice. Managed money is also signalling they don’t believe that we avoid a recession. You’d expect to see active cash in short dated money market accounts start to taper, preferring longer term yield instruments (this chart only shows 2008 as a correlation, which is a shaky one owing to the speed at which the FFR was cut to zero), that hasn’t happened. If the incremental energy buyer is under the impression we slip into a recession in 2H23 or even 1H24 — zero chance they are buying energy right now.

Cut the free cashflow, and then really, nobody wants to own resources. The majors (plus CNRL so us Canucks get some representation) have been floating around 12% free cash yield for a few years now (money market is now ~5%) and for a year have been returning to shareholders, most of that cashflow. Even pre-COVID, CNRL was a double-digit free cashflow yield — and nobody outside the sector batted an eye.

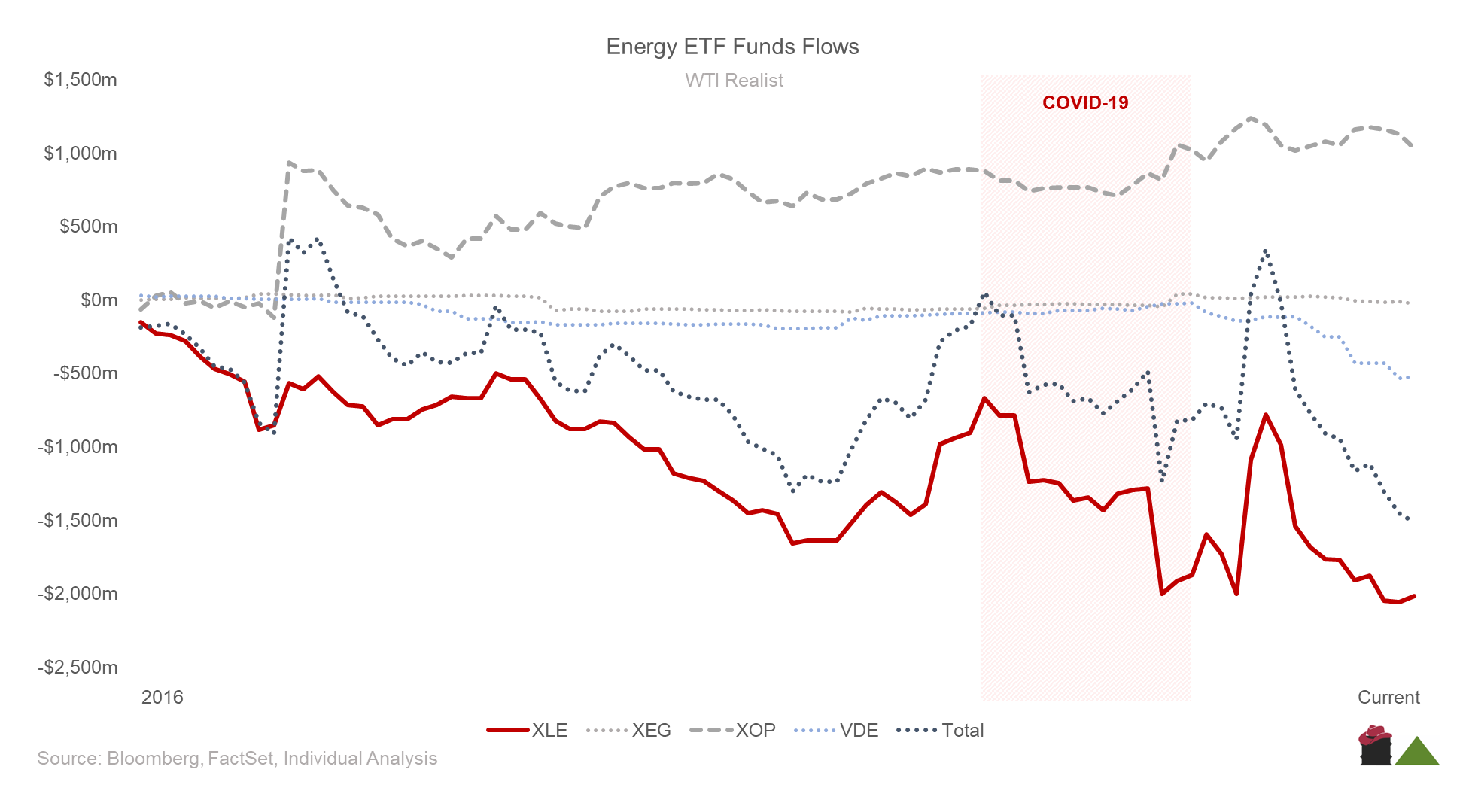

The concern now is — energy stocks are cheap (relatively) sure, there’s no doubting that. Paying 6x free cashflow for a well run E&P is a good price (key here is well run), though the market wants absolutely nothing to do with them. Since 2016 (and I felt that was an appropriate baseline as it was clear from 2014), various energy ETFs have seen almost $2bn of outflows — and while the XLE in May had almost recovered to their pre-COVID AUM watermark, they just missed it, and today sits at cycle lows. Nobody wants to own energy here — and you need someone to bid your equity up if you want any sort of meaningfully durable rerate (otherwise it’s just me and you passing the same shares back and forth all day).

Interestingly enough, explorers still have some bid here, which may suggest there is some appetite for risk, though a niche part of the market as it stands (perhaps people more desire torque to the trade, than they do actual exploration).

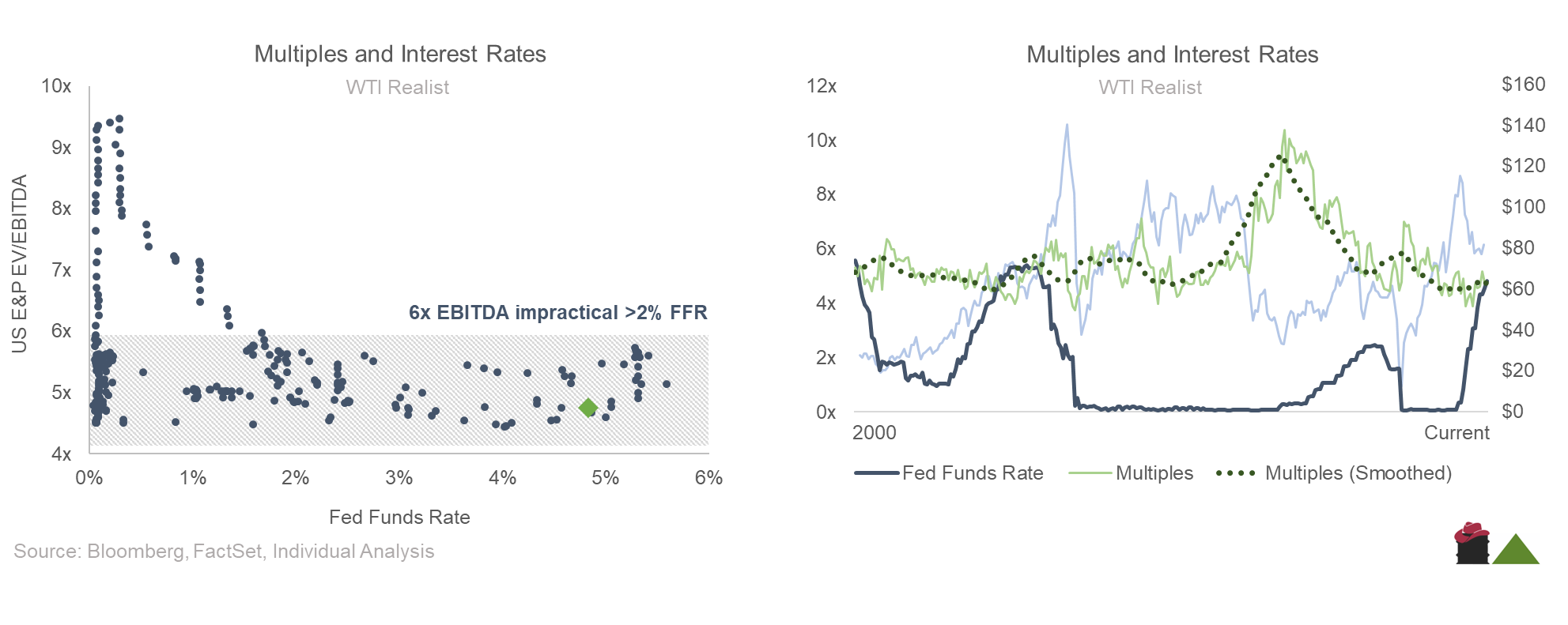

The entire kicker here is we need, as an economy, to digest a recession — you can feel the tension across the nation before we get unemployment numbers — you’d probably rally on higher unemployment, but that’s besides the point. Market participants think a recession is coming, which makes energy entirely unownable for most capital out there. It’s two fold — you likely don’t see a quick cooling of interest rates until they break something by hiking too fast, and if you do see a recession, the inevitable oil price softening will (presumably) kill equities. Yes — I know oil (price and demand) can go up throughout a recession, but we are thinking like realistic generalist allocators here (who we need to buy our equities), they are not underwriting any serious possibility of that occurring. So — until the economy rolls and you have a clear line of sight to recovery on the demand/price side, most people aren’t going to touch energy. Then — multiple wise, it’s simple math — the higher return you can earn risk free, the less attractive risk looks.

We’d be kidding ourselves if we said energy wasn’t a risk asset. So you have a cap on multiples (pretty much 6x EBITDA is your ceiling, and we hover at 5x right now across the US E&P universe), if you’re uncertain on where the economy goes. That puts energy at the bottom of your list.

Then (and this is where those changes come in), on the other side of a recession (sorry free cashflow lovers) you’re going to see some free cashflow get reallocated from shareholders, to the development of resource. Some of that may be financed with debt (don’t expect much equity this go round) and better balance sheets means that you won’t really see negative free cashflow, but you’ll see a hit to free cash yield. Now — better balance sheets also mean that most businesses can support some healthy leverage in a post-recession up-cycle; but that also means they shift from focused to return of capital, to return on capital. You should know (or at the very least have an idea) of what that looks like for the names you own.

See below — as multiples rise, free cashflow (inverted here) goes negative; and vice versa. Multiples are at all time lows, and free cashflow is at all time highs. Yes, we are in a steady oil price environment, but ultimately the multiple is how many years you want to pay for the earnings, and being essentially in no-growth mode, into a backwardated strip hasn’t really made most E&Ps (more just Ps now) that compelling.

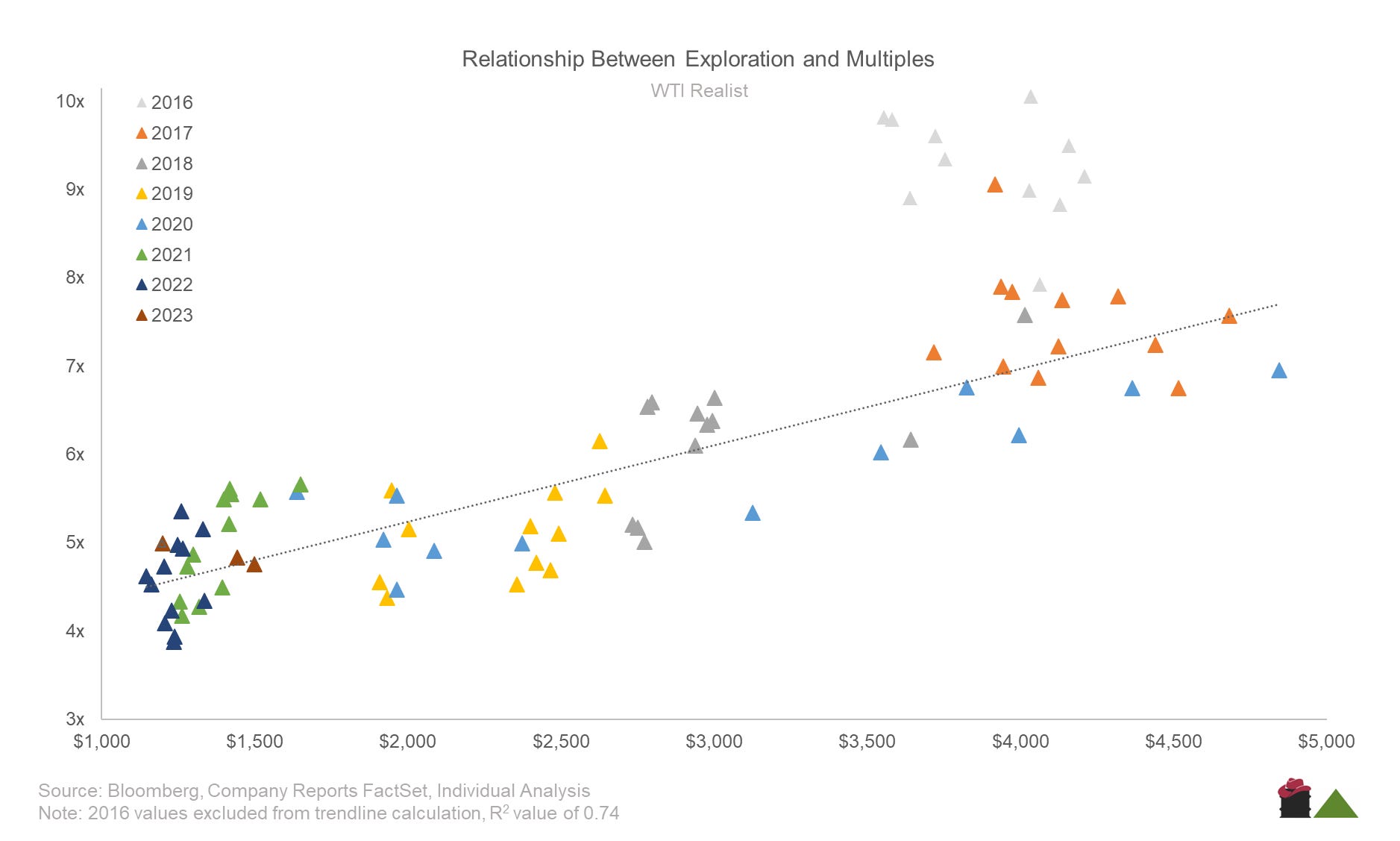

You just can’t have a higher multiples without spending some money developing your assets. it doesn’t have to be exploration, but you have to do something to expand the value of your business. After all, if you are clipping 20% FCF with no terminal value (or a very capital intensive terminal value) — you should be paying maximum 5x FCF for that business (and in reality, far less). The issue is the constant push for return of capital has encouraged management teams to do the bare minimum. Now, this isn’t something I believe is a global supply issue (these are tiny players, still growing at a reasonable pace, but we will discuss that in 3 minutes), more a health of the general business issue. If you starve anything of capital, you’ll see sky high free cashflow for a few years… they say something about every reaction having an equal and opposite one; that’d apply here. You need to create some sort of shareholder value.

By the way, paying a 10% dividend isn’t creating shareholder value.

So — for now we are just humming along, all collectively waiting for some sort of signal the economy is either going to stall, or we’re okay for now. Both management and capital allocators too — from management’s perspective, why drill now into a 2x DACF multiple — and from a money managers perspective, why buy something into a totally uncertain macro. It’s a stalemate.

The remaining 2/3 of this article is for founding and paid members. Please take advantage of the promotional offer below should you wish to support my publication.