The Best Way to Play Gas Isn't in BC

The Best Way to Play Gas Isn't in BC

It’s no secret that natural gas in North America is in for a rough year, the Henry Hub cash contract is down 40% since the start of the year, and over 70% from the highs of 2022, and AECO is in a similar boat. While the natural gas weighted equities have shown some resiliency thanks to the back end of the futures strip holding up (you do have to have some semblance of a long term view when buying gas here). Volatility in near-term pricing should lead to great opportunities to add gas weighted equities at intra-cycle low valuations.

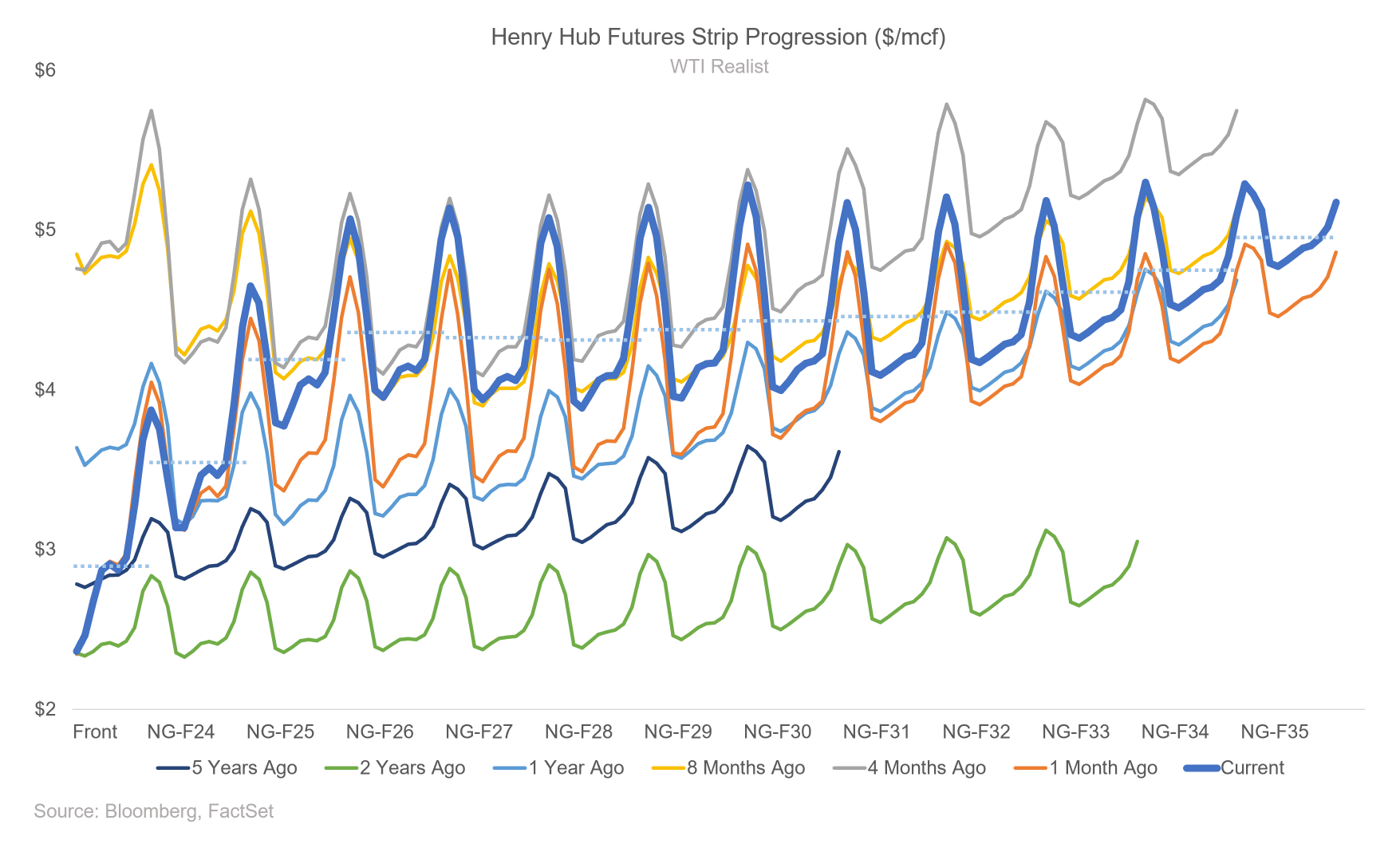

While the balance of 2023 (average, for Henry Hub) is <$3/mcf, the balance of the decade is closer to averaging $4/mcf. Certainly not an awful gas price compared to the prior decade, but not immediately intriguing at today’s equity multiples. As the spotlight on gas development has slowly shifted west (remember when the Deep Basin was all the rage) into the Montney, the few remaining dry gas producers in Alberta, and Saskatchewan have slowly been ignored. After-all they are not sexy when compared to condensate rich IP30 rates of 1,500boe/d. Nonetheless, this doesn’t mean at the right price their stories aren’t intriguing. Pine Cliff is one of those companies that people kind of forget about. It’s not really a major LNG name, not a takeover candidate, and isn’t in any of the indexes. It does run a solid business and pay a great dividend though.

Equities have certainly followed, to some extent, the slide in gas prices, but into summer volatility, there is likely some downside. As the front of the gas curve leads equities lower, there will be days to average into quality names that are “taking it on the chin” less than others. Pine Cliff is one of them. Of course, the key here is to have a personal thesis backed by a stronger curve in future years (2024 winter).

On a “gas glut until additional takeaway is in place” view, it’s harder to get excited about Pine Cliff at this price— it’s a good company, full stop, and like many others in the patch (Bonterra and Journey come to mind), they have humbly played the hand they’ve been dealt, unfortunately, this year they have been dealt weak gas prices. While some names are great vectors for 2025-27 fundamentals (think Montney development focused vehicles), Pine Cliff is less so an apt way to express a long term WCSB gas view. While LNG can be exciting (to some, not me), you’d be hard pressed to really make the pitch that Pine Cliff benefits from LNG in a fulsome way (other than less volatility in the local benchmarks), though that’s neither here nor there.

While other “value” gas peers would be in the “danger zone” for one reason or another, Pine Cliff is in a place they can wait in low gas prices for a few years without materially altering their business through cutting capital for development and abandonment, or cutting their dividend. While there are other peers (namely Peyto) in a similar spot, Pine Cliff has a load of cash on the balance sheet, and their unique “little downside, high upside” torque proposition is doubly attractive. Even on an unhedged basis (though their continual hedging strategy is to protect the summer and participate in the winter) with a ~$3/mcf AECO breakeven, if low prices persist through 2024, your downside on a target buy of $1/sh, theoretically is much less than a Peyto or Birchcliff.