OPEC Pre-Meeting

There is a lot of discussion about what may happen tomorrow, and what OPEC decides to do with their production quotas — cut, or maintain. Feel free to read my discussion after the previous meeting (note post-OPEC+ meeting in April) — while many of the same longer-term themes still remain — continued downwards pressure on oil prices have been a consistent theme since the last meeting, and the Kingdom has certainly shown disdain towards crude traders perhaps not providing a futures market conducive to the type of price discovery that OPEC wants. The crux of this meeting, and really the cartel, is to manage the price in a way that fits their long term thesis. Certainly — the OPEC member States have a similar long-term thesis as a lot of those in the commodities trade — oil gets harder to find at low prices as time rolls forward, and demand is harder to replace than greenies would like to accept.

Though 2023 has made the trade much harder, even confusing — global inventories are building while China is reopening, and while OPEC has communicated two top-line cuts since May 2022’s oil peak (one in October of 2022, and another in April of 2023) — oil prices have continued to fall, in what has been generally accepted to be an already tight market. While inventories have been rising (even with the long-awaited additional Chinese demand), working against the long peddled narrative that there is an incoming oil ‘super-cycle’. While the supply and demand fundamentals are certainly encouraging, as previously discussed, the idea of a ‘super-cycle’ is somewhat contradictory in of itself, simply due to the amount of economic inventory at ‘super-cycle’ prices. Either way — I digress, the unspoken objective of this meeting, is to put some sort of pressure on the general market, without seriously compromising fundamentals of the next 12 months — not an easy task. The overwhelming consensus of a ‘tighter’ second half for the oil market, is something I would generally agree with, so any serious cuts (that aren’t just quota decreases, a shuffling of capacity, or a redefinition of the baseline) — only serves as further risk to OPEC as an overly tight market not only breathes needed life into marginally economic production (i.e. most of the United States), but it also puts them at risk of further global strategic inventory draws.

So — you need to do some pretty skilled tightrope walking here. Something that inflicts short term pain to speculators, a move that doesn’t overly tighten future months, while (hopefully) improving strip backwardation to a point where there is some incentive for participants to treat oil like something more than a silly little risk asset (which in of itself would preclude anything crazy).

But from the market’s point of view — really anything OPEC will do, is likely to be wrong. Actions too brash that push the 2H price too high is likely to be dampened by increased US production outlook, with a higher probability of a recession to boot (and the acceleration of the implied demand destruction associated). Cuts too soft may let the market down, and nothing at all would quite possibly be the worst outcome — serving only to prove the lack of seriousness among the cartel.

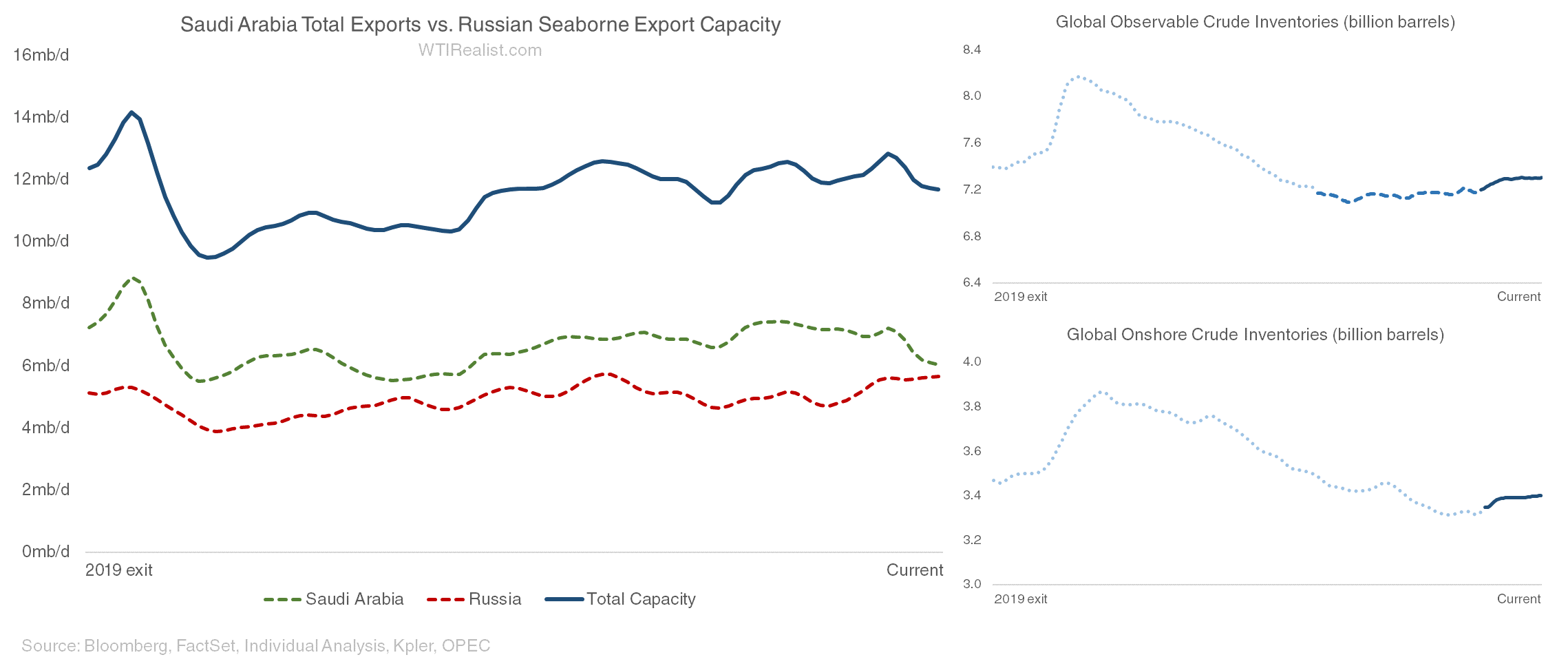

Nothing is as important as further clarity on Russia’s position. Since the two rounds of cuts, oil exports between the two largest OPEC+ producing nations (Saudi Arabia, and Russia) are effectively flat. While we can wax and wane over the base month, over the past year, essentially, combined exports are up. Without structure, or even further detail as to how Russia will be handling April’s voluntary cut — any actions from the OPEC core members will be marred and deemed inconsequential.

Such is the issue that OPEC faces — keeping Russia in check — without compliance from the Federation, really, anything that OPEC does can be easily offset. Further cuts from core members are less than ideal (if not a sign of weakness).

Ideally, from a price (rather than production) standpoint, you need to put some backwardation into the curve (which is not kin to permanent/long term cuts). Not only to make it cheaper for money managers to be long crude (through higher roll yield), but strengthening the front months while leaving the out months relatively stable serves the double purpose of kicking shorts in the nuts (as open interest in really anything past 2023 is nothing).

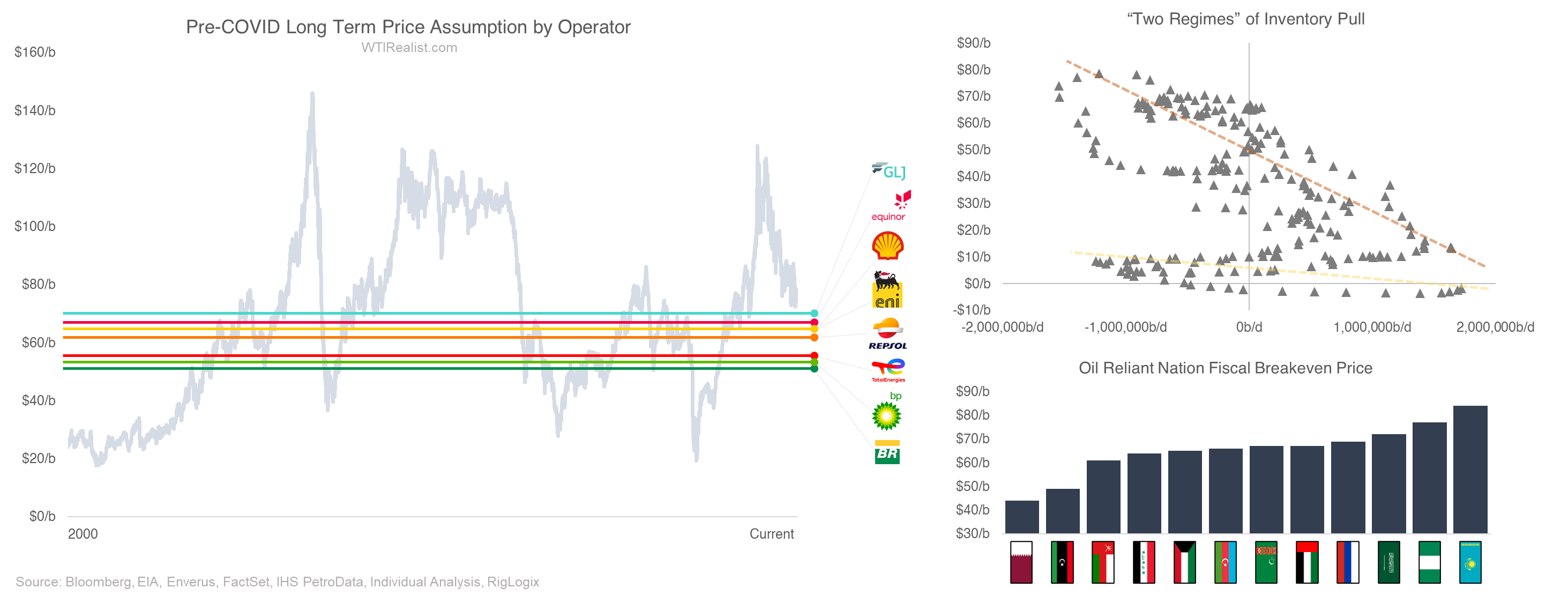

The struggle with backwardation, is you need to manage the price to a point where the out months aren’t so low that there is a discouragement for actual supply adds. Recall the slide from last week’s note, where the long term price for profitable supply growth outside the United States is somewhere in the $65/bbl Brent range. If OPEC can successfully keep the 2026 and beyond contracts where they are, while lifting the interim contracts higher, they’d (in my opinion) have succeeded. That keeps roll yield high for managed and leveraged longs, benchmark prices near fiscal breakevens, and importantly, puts the world in a “yellow regime” with respect to pricing sensitivities to inventory movement. The “orange regime” is one where the market is highly sensitive to implied balances, where the source of incremental production is unknown and/or demand is growing rapidly (dates sampled include the 2010 run, 2006-2008, and 2018-2019). The “yellow regime” is where there is spare capacity, and less pandemonium in the market — it’s a pricing regime that is much better for OPEC.

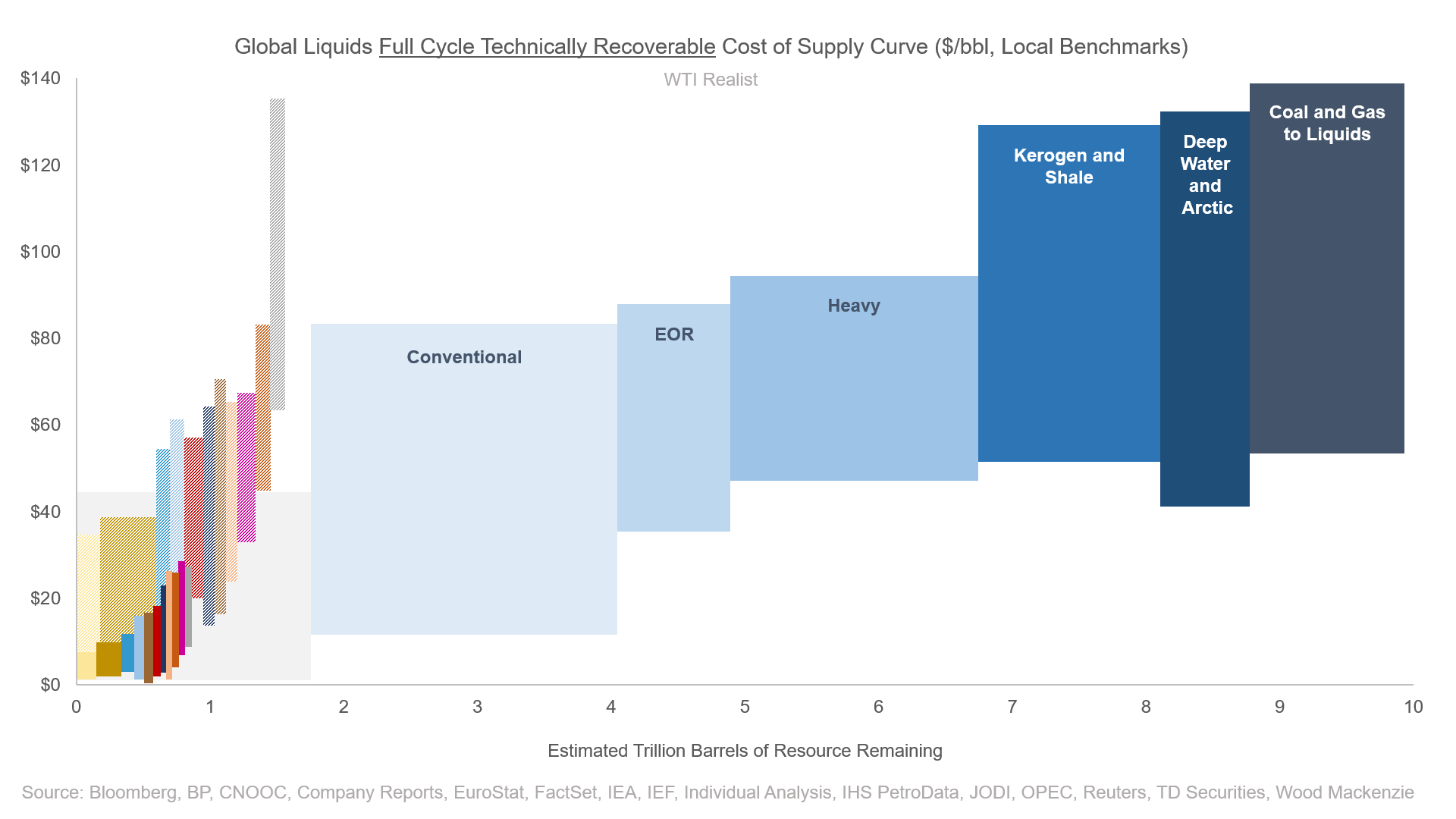

Back to my capital cycle note — the general idea, that I think OPEC should target, is a slow unwinding of spare capacity for a slow increase of prices. The important note here, is that if you want to truly be the marginal/swing producer, you need to keep benchmark prices where enough global production (and enough production for say, the next 5 years) is economic, but prices aren’t high enough that everything works.

Which is why I think if OPEC really wanted to do what they want to do — they’d increase production, and move prices down to a place where they are the marginal producers, where shale barely works, and where they can essentially influence rest-of-world supply through the maneuvering of spare capacity. It would flip the script from “call on OPEC” to “call on the rest of the world” — but of course, that would be a monumental change in oil market dynamics and unlikely to happen.

Because the thing is — OPEC does know there is a ton of supply (and thus they absolutely cannot let prices stabilize higher, as they lose market control again).

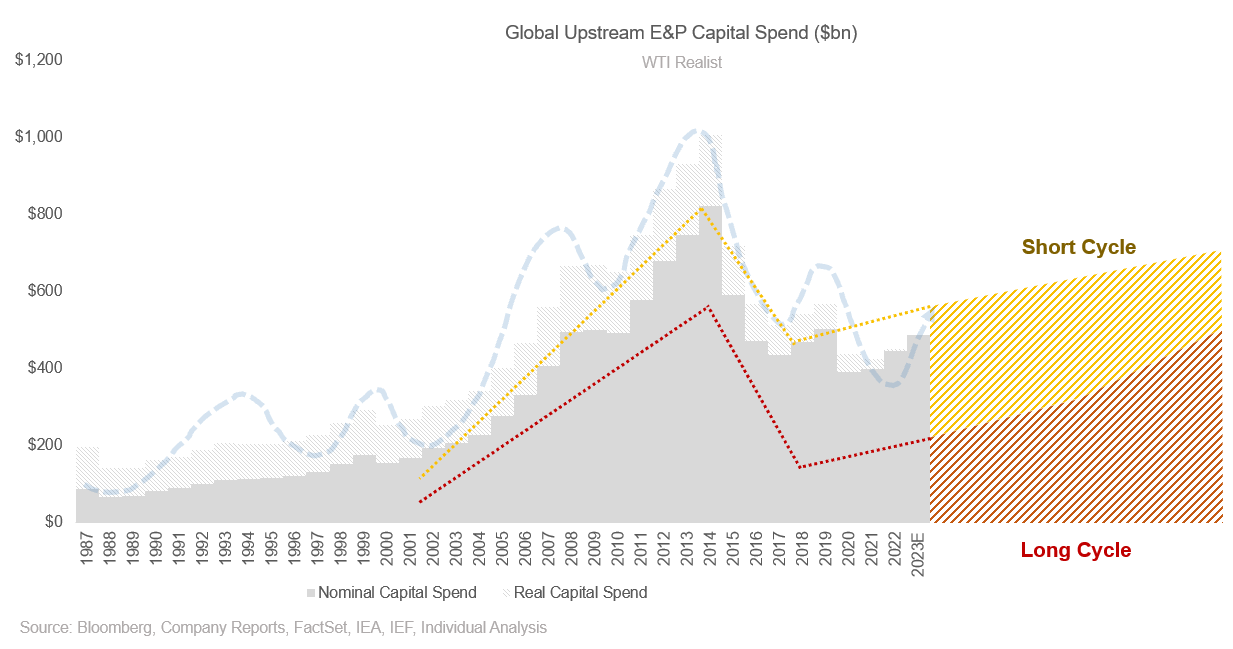

Instead of short cycle projects that only work to dissuade long-cycle investment (i.e. all of the United States), targeting a price that makes sense for long-cycle producers, without flooding the market with short-cycle oil is ultimately, where I believe OPEC needs to land, and why I also believe they won’t let the price get too out of control in the second half, as it gives strength to additional short-cycle production.