Ju-n-ior Own Out Here

Ju-n-ior Own Out Here

Now isn't the time to hang out down market

I have said before, perhaps to the chagrin of those ‘in the ring’ — that the energy game, at its core, is simple. Buy names that can add barrels for cheap, then produce those barrels with a strong margin of safety. There are overwhelmingly few companies that have succeeded to do just that, you could probably count them on one hand.

Junior companies are great, and typically need an interesting story, otherwise they wouldn’t compete for investor capital — naturally capital eventually migrates (through way of high-grading, or inorganically through acquisitions) to those names with the strongest track records, and most consistent returns (which, happen to be, in general, the most expensive). Thus, the industry’s recent delirious focus on “return of capital” over encouraging companies to do what they should do (that is, explore for hydrocarbons), has left for little differentiation between cap sizes. I get it, multiples aren’t high, and you certainly aren’t rewarded for growth — which is the whole point of a junior name…

So, where is there room for a junior in the portfolio? If they aren’t differentiating themselves via growth, and have more volatile track records when compared to the now monumental majors — what’s the incentive to go down market in a price environment that doesn’t feel extremely constructive.

If we hang around $75/bbl on the WTI benchmark, well, junior producers are in a tough spot, while there is still plenty of breathing room for the higher quality names. Junior names retain strong exposure to interest rates, especially those that took the previous year as an opportunity to re-add leverage to their balance sheet (super cycle anyone) — along with possible negative differentiation thanks to higher ARO balances, operations which are more capital intensive, less ability to effectively take advantage of A&D at cycle lows, payout ratios above 100%, and, just in general, attributes that don’t exactly scream “pick me”.

So now the question, in my mind, is when does apathy for the energy trade kick in? Though it would seem sentiment is strong on Twitter, shockingly, resource investors exist outside of the internet, and there’s no doubt that junior resource investors are getting a bit tired of being sold a story that hasn’t materialized. Now, I’m certainly not calling time of death on the energy trade, but there is a reason that non-institutional investors are not called “smart money” — they flop in and out of trends, and, well, often lose money. Energy is no different. While energy hopefuls were pitched the idea of a super cycle pushing prices to $250/bbl — what has materialized is much different, and junior names, the ones with “torque” will slowly be crawling towards -50% y/y change as we move into June. While the S&P 500 is up 8% YTD, and the XLE is down 7% YTD — that’s not the worst of it — the NASDAQ is up almost 30%. Growth has been dominating the markets so far this year — while the “energy as an inflation hedge” story has fallen flat on its face. To add insult to injury, oil inventories have been drawing, and producers cutting production — no dice. I believe, like most others, those that decide to be disciplined about their energy allocation (and, to be fair, that includes being smart about junior investments) will be rewarded, but it’s certainly exhausting to be an energy investor — and we haven’t seen capitulation, yet.

While some days this year may have had you scratching your head — crude up, stocks down, or crude down yet equities rallying — when you normalize it on a rolling weekly basis, there hasn’t really been any unusual activity, on all three major North American indexes, the XEG, XOP, and XLE. The explorers index (XOP) has traded pretty much exactly in line with the capped indexes (XLE and XEG). If you were looking for clear signs of capitulation in the correlation you’d want the markers to drift into the lower right quadrant, where equities are selling off while there is some strength in crude — we haven’t seen that yet — and it’s possible we will, and my bet is on weakness as owners of junior equities clue into their poor performance, and decide to move up-cap and high grade, or switch out of energy all together.

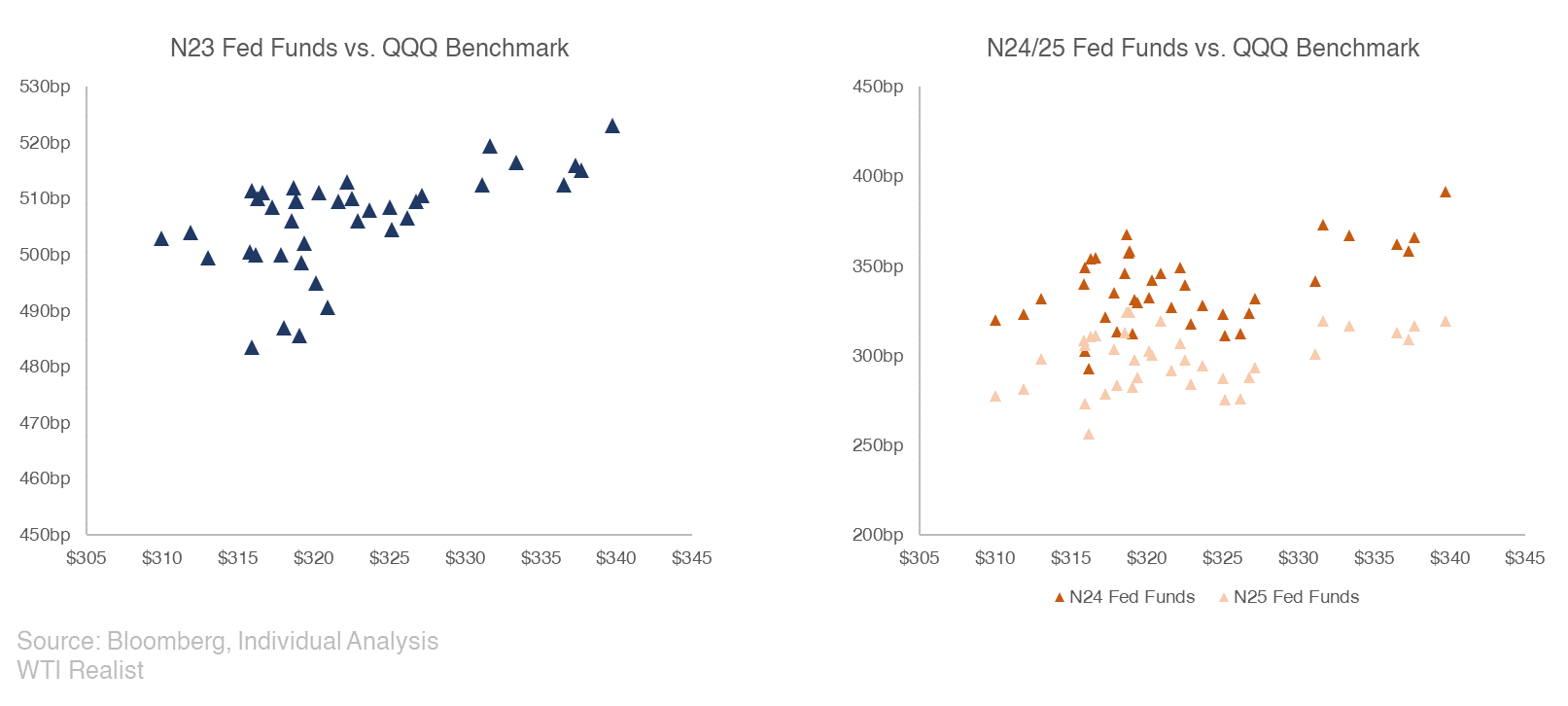

Before we really get into things — a word on the market going parabolic — such strength in real economy numbers, and in the financial markets, unfortunately drag interest rate expectations (and likely interest rates) up with it. As we’ve seen the QQQ move up 10% from $310 to $340, we’ve seen July rate expectations move up from 5% to 5.25%, and “higher for longer” (and not the “higher for longer” the oil bulls were hoping for) persist in the out-months of the fed funds futures curve, with the July 2024 rate expectation gaining almost a full percent, and July 2025 moving up 60bps.

The implication here, is as you push rates higher, prevailing sentiment turns into “we keep going until something breaks” (which means avoid energy), and if rates keep pushing higher with apathy towards oil remaining persistent (see net crude positioning right now, at pretty well all time lows) the interest cost for a number of junior E&Ps with floating rate debt becomes noticeably higher, and for those E&Ps that added termed leverage with maturities coming in 2024, or even 2025 — higher for longer interest rates at $75/bbl means being forced to refinance debt unfavourably. It’s kind of a catch-22 the way that I see it.

The move in the yield curve, and the LIBOR curve, has some serious effects to junior and micro E&Ps that are borrowing on floating facilities. In some cases, a 1% change in interest rates, means an additional 1x on your ND/EBITDA ratio — which further hampers any hope for a re-rate.

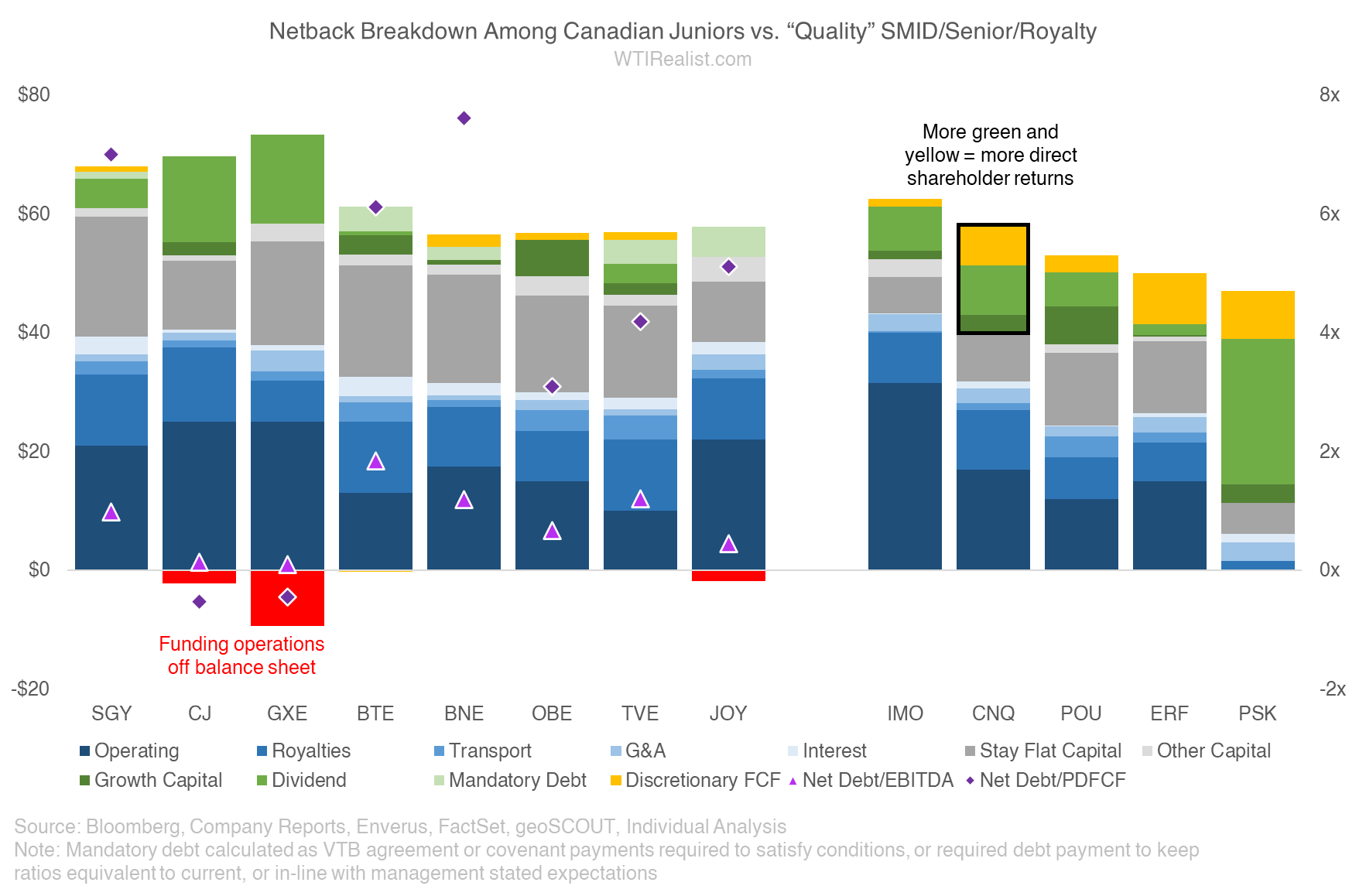

So, let’s get back into it — junior names, full stop, don’t have a lot of flexibility right now. Either they have handcuffed themselves to a dividend (CJ and GXE), are high cost operators (JOY and SGY), or capital intense (BNE and BTE). The unfortunate part about those that generally do okay in each of those categories (mainly, BTE and TVE) is that they have added so much leverage to the balance sheet over the past year, that they have to be laser focused on executing their plan flawlessly, and any missteps would be incrementally, very negative. While these are certainly businesses that you can own, they don’t feel really ownable right now, given sentiment and price trajectory.

The remaining discussion is for paid subscribers. Should you wish to become a member, please follow the link below.