2H23: Not Out of the Woods

2H23: Not Out of the Woods

16 things I'm thinking about

In again, another deviation from my usual focused exploratory work (which is not going away, by any means) — I write to everyone on vacation, with a summary of my key themes going into the second half — ideas to consider, on a macro, and equity level, and generally, what I am thinking about oil markets (and I hope, that’s why you subscribe, though, fodder to make fun of me, would also be valid). So behold, a collection of thoughts, from me, for you to consider, explore, inquire about, whatever you’d so like. This is scriptum ex-laptop, so forgive the degradation in graphic quality.

The main theme, is, we’re not out of the woods. I am opimistic for the second half of the year, but I have long posited, that we are back in a normal crude market. The note below, is a good refresher of how I generally think about the market, and my mental handbook to the liquids capital cycle — I am not a believer in sustained $100/bbl oil, and especially not in 2023, and below outlines some of those thoughts.

Enough of the chatter — 16 of my talking points, and headline thoughts that are guiding my positioning, and advisement for the coming months.

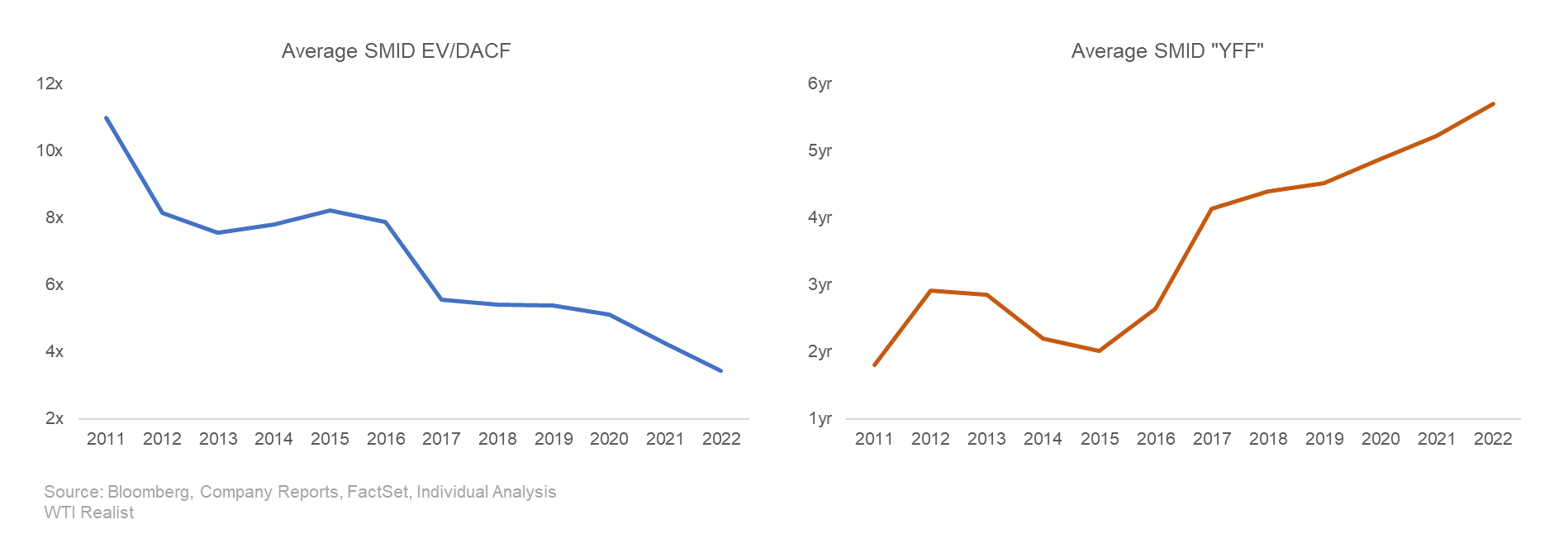

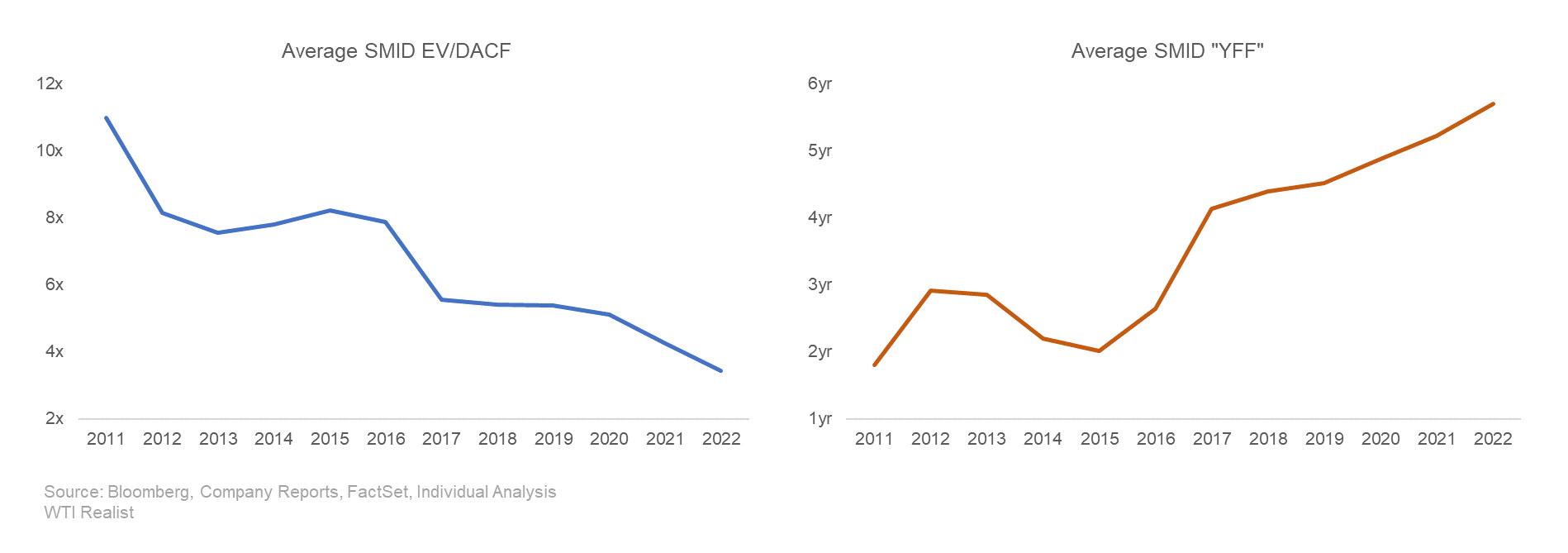

Multiples, still relatively stable, not so cheap when reframed. While yes, multiples are down from 10x EV/DACF in 2011, we’ve also drilled through a decade of inventory during that time period. While Canadian’s laugh at shale for depleting their core inventory first, it’s not really much different here. The fact is, there’s less easy oil in the ground (hell, there’s still a lot of it, and lots that isn’t booked), but when you reframe the multiple, as “how many 'years for free’ do I get” (with respect to 2P inventory), really, you’re only getting less than 2 more years for free over 2017. The whole “cheapness” thing, was a trend that started in 2016. When you think that, for the most part, good inventory is now harder to come by, we aren’t sure what happens with carbon tax in the province, and we are closer to ‘end of life’ than we were a decade (or even 5 years ago), it makes sense that you get 1-2 years more of inventory for free. Lots of ways to look at things, but note, incremental buyers that represent size are not simply looking at a 2011 EV/DACF and deciding to fill or kill at open, they are (for those that I’ve worked with), interested in adjusting for more qualitative metrics, and when you start to adjust for those, you kind of see valuations start to level off.

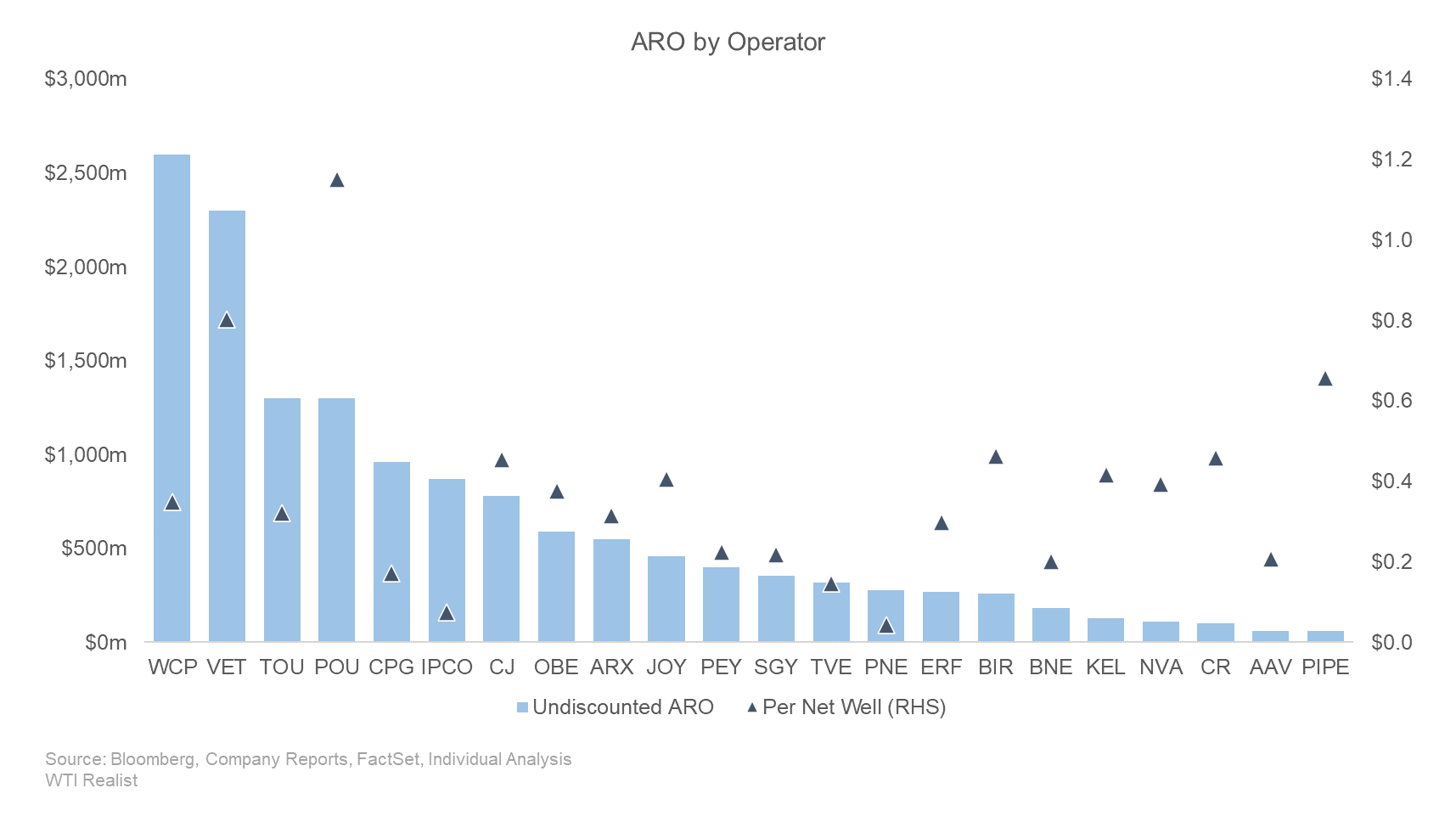

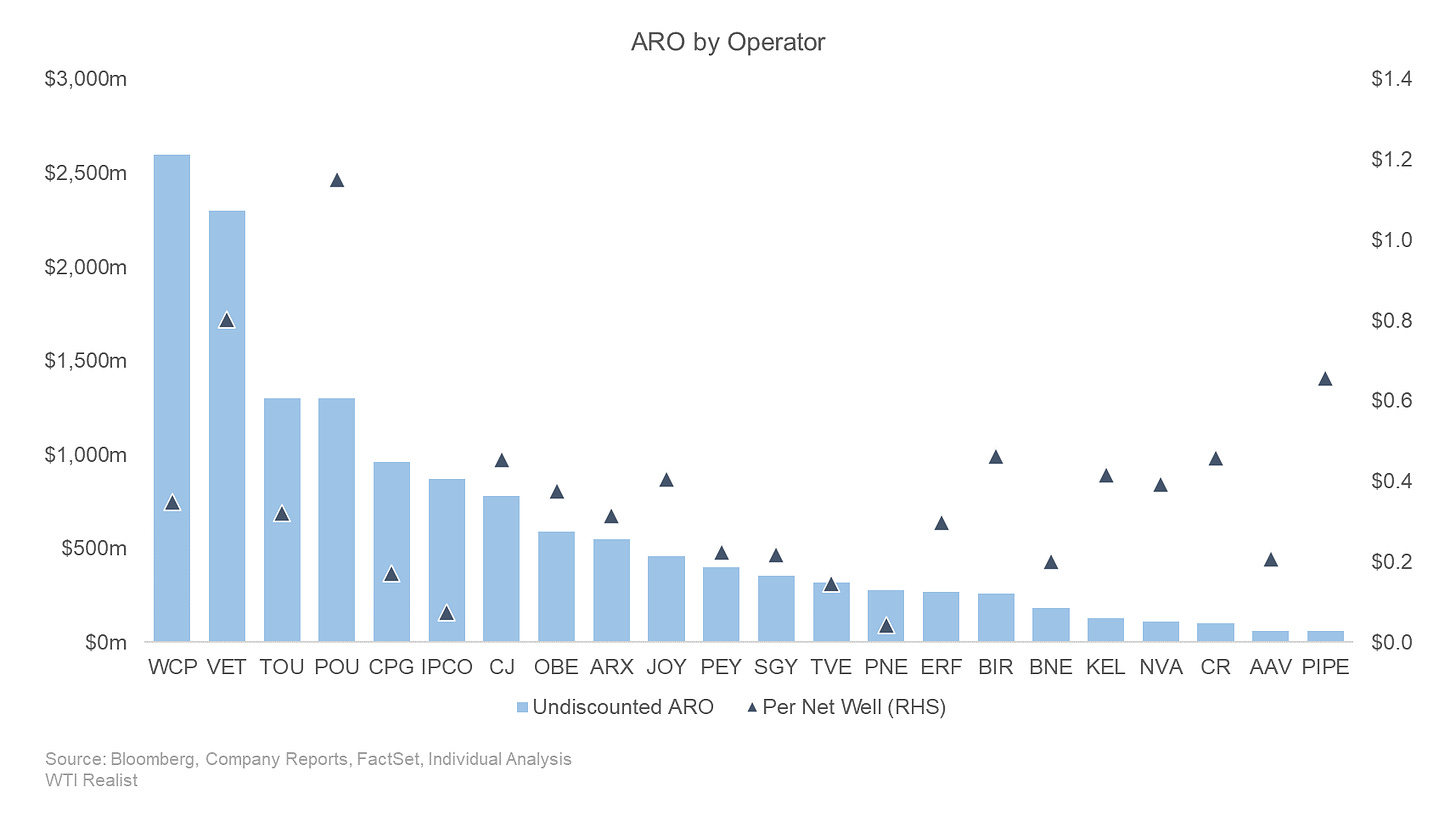

ARO is a concern — commonly, the thought is — kick the can down the road, and discount it out (a bit hypocritical that a company would use a credit-adjusted discount rate on their ARO, but a market standard NPV10 on their reserves). Generally — the common attitude is to just ignore it, which I don’t agree with, considering, aside from commodity price decks, it’s the most impactful thing to shareholder returns over the next decade. There’s a huge incentive to underreport ARO on the corporate level. I am not suggesting this happens, or is common, but there’s an obvious misalignment of incentives between management and shareholders. Management wants to understate the liability, and shareholders, generally should want to know the full impact, as, even if it may not seem like it, something that’s monumentally important to the whole future free cashflow the company will generate — which is pretty central to the whole public equity pricing thingy. Wether we like it or not — “this time is different” applies to the potential carbon emissions, and ARO obligations of E&Ps — though, this time it means that chunky incremental funds flows will be paying attention to the environmental implications of their investments, alongside business returns. Different from last cycle, and the cycle before, where cash on cash returns were headline, and environmental obligations were little discussed. This is a post-Redwater decision cycle, and that is hugely impactful, and I believe not understood, or appreciated by current market participants. Incremental equity flows are absolutely demanding to understand the asset retirement, and emissions profiles of these E&Ps, and among a handful of clients, a “make or break” decision when it comes to allocating capital into these companies. This isn’t an immediate “on the clock decision”, but something that I think everyone needs to have a plan for, decide what is “priced in” — below is a chart that shows undiscounted ARO by operator (doesn’t back out infrastructure on a per well basis) — this is a number that greatly impacts terminal value. No, you can’t call for a rerate to 10x without understanding this part of the business.

If you wish to become a paid subscriber, along with 10% off, new subscriptions come with an extra two months (annually), or a free August billing cycle (monthly), as I take some time off during July.