2023 Vibes: Vermilion Energy

Vermilion Energy is going to generate a lot of free cashflow over the next 36 months. Much less than expected at the peak of TTF gas pricing, but nonetheless, they will have ample FCF to spend in excess of capital requirements, and their dividend. I am not here to argue that. Though, in my opinion, expecting an 8x FCF multiple (would map to approx. 5x EV/DACF) is not only lazy, it’s misleading and trite. I have seen some incredibly poor, lazy, and frankly intellectually dishonest work done on Vermilion in 2022.

Vermilion is an international energy company, and thus, carries increased risk compared to Canadian focused peers. This additional risk, along with their perceived over-earning status, in my opinion, is correctly reflected in their lagging valuation. This lagging valuation, paired with what I expect to be earnings disappointments over the next year, will see Vermilion at best, flat, with major risk to the downside. I would be buying Vermilion as a proxy to express a view on higher TTF gas prices— though as an energy company, there are better options available in the market.

To The Upside

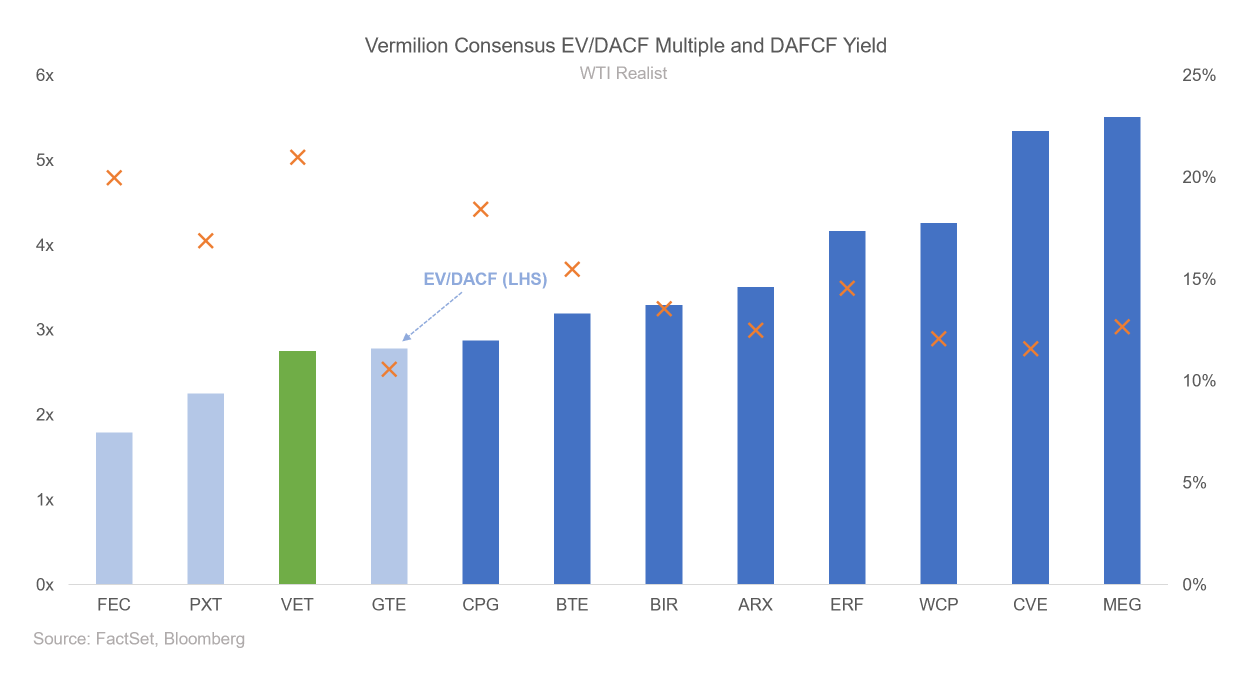

Vermilion is cheap. There is no denying that on an EV/DACF basis, and even a debt-adjusted free cashflow (DAFCF) basis, they screen as cheap, if not the cheapest, among peers. If you believe that they can continue to execute in North America, and leverage their European gas position to pay special dividends, they should see some manner of re-rating over the next few years. They have what I might describe a wide jumping off platform, there are many avenues of their business where they could theoretically create value. If they can successfully execute— less than 3x DACF is a great price for a solid business.

Their windfall tax scheme (potentially) rolling off in 2024 is also a strong catalyst to the upside— lower gas prices mean a good read through on the duration of the windfall tax which is currently impacting their international revenues significantly. A positive guide on the windfall tax regime from with the EU governments, or Vermilion themselves would likely translate to a few extra points of market capitalization, given their multiple and current tax expectations on strip pricing.

Constructive guides on their Montney development pace may also have a positive read through for 2024 and beyond cashflows. Their corporate volume estimates have come off as international production has softened, and future, expedited Montney development could lead to beating expectations in 2024 and beyond. Recall they already have permits for facilities for pads at their asset acquired with the takeover of Leucrotta Exploration— as the effects from the Blueberry River First Nations agreement are ironed, they also stand to incrementally benefit sentiment wise, though none of their lands were directly in protected areas, or majorly in jeopardy of being detrimentally affected by the BRFN affair.

Finally, their Australian oil production, which sells at a premium to Dated Brent, should not only provide support to their average price realization, but production growth in the area would also be a positive. Think to the first chart, where their expected realization per boe is now half of summer consensus. Further oil growth, I believe, would be very much welcome versus more European gas growth.

To The Downside

Their 4Q22 print will likely be light on cashflow compared to their 4Q21 print, due to approximately equal TTF pricing, though a new windfall tax which will begin being booked in 4Q22. This may finally jog the rest of those holding hoping for improvement over 3Q22, that it’s unlikely to come.

Expect the focus to switch from a play on TTF gas beta, back to what their development and business plan is over the next few years, i.e., a shift back to management and their outlook. I believe this levelling of TTF prices through the spring and summer, and their debasement from being a beta play, should bode negatively for the stock, and people focusing on assets and execution will favour other names. See below, a chart where we can adjust for value destroyed during previous cycles. Vermilion does not screen well on this chart, and when the earnings from European gas roll off, they move solidly in line with where one would expect them to be. Other names on here like TSX:CPG, TSX:ATH, or even TSX:SGY make more sense as actual businesses than Vermilion at these commodity price levels.